Management's Discussion and Analysis

Analysis of Financial Statements

The USGS consolidated financial statements are prepared in accordance with accounting principles generally accepted in the United States of America as set forth by Federal entities, guidance issued by the Office of Management and Budget (OMB) and the DOI. The DOI Office of the Inspector General (OIG) is responsible for auditing the consolidated financial statements of USGS and has contracted these services to KPMG LLP. The audit of the FY2003 consolidated financial statements is limited in scope to the Balance Sheet as of September 30, 2003. This financial overview of the FY2003 consolidated financial statements contains highlights of significant balances contained in the accompanying consolidated financial statements.

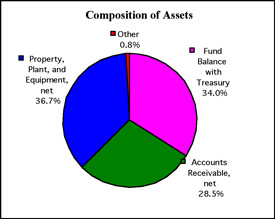

Composition of Assets

The Fund Balance with Treasury of $205,258 represents 34% of total assets at September 30, 2003. The Fund Balance is primarily composed of appropriated funds available to make authorized expenditures. The USGS working capital fund comprises 41%, or $84 million, of the Fund Balance with Treasury.

The Fund Balance with Treasury of $205,258 represents 34% of total assets at September 30, 2003. The Fund Balance is primarily composed of appropriated funds available to make authorized expenditures. The USGS working capital fund comprises 41%, or $84 million, of the Fund Balance with Treasury.

The General Property, Plant and Equipment (PP&E), net of accumulated depreciation, amounted to $222,126 at September 30, 2003. This amount includes a satellite reported on the balance sheet at a net book value of $75,664, as well as land, buildings and improvements, furniture and equipment and software purchased for internal use totaling $146,462. The satellite transferred to the Bureau by NASA in FY2002 represents 44 percent of the value of the Bureaus total equipment. During FY2003, the satellite experienced technical problems and is currently operating in a diminished capacity. As a result, the satellite's value was reduced by $81,100 and an impairment loss was recognized in the Statement of Net Cost for the same amount.

The total accounts receivable of $172,521 is almost equally divided between other Federal agencies and the public. The majority of the accounts receivable is established to cover the direct and indirect costs for reimbursable services performed in support of surveys, investigations and scientific research. The majority of the receivable balance is unbilled. 92% of the $81,089 receivables from Federal agencies are unbilled. 71% of the $91,432 receivables from the public are unbilled. The large unbilled balance is due to the manner that agreements are written for survey and research type work. The revenue for an agreement is recognized as work is completed, but the receipt of payment is often not due until completion of a survey, or research report, is completed.

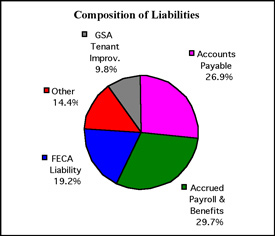

Composition of Liabilities

The USGS is a scientific service organization, where the majority of its liabilities are for accrued payroll and benefits. The accrued payroll and benefits and annual leave amount of $78,732 represents 30% of USGS' total liabilities of $265,188. The accounts payable of $71,363 consists of $8,940 accounts payable with other Federal agencies and $62,423 accounts payable with the public.

The USGS is a scientific service organization, where the majority of its liabilities are for accrued payroll and benefits. The accrued payroll and benefits and annual leave amount of $78,732 represents 30% of USGS' total liabilities of $265,188. The accounts payable of $71,363 consists of $8,940 accounts payable with other Federal agencies and $62,423 accounts payable with the public.

Deferred revenue and credits of $15,751 consists primarily of amounts advanced to the Bureau to cover reimbursable services to be provided at a future date. The deferred revenue with federal agencies of $35,914 in FY2002 has been reduced to $2,835 in FY2003. This is a direct result of the implementation of common business rules for intra-governmental transactions that ended the practice of taking advance payments for service orders with other federal agencies.

Unfunded liabilities with a balance of $169,668 make up 64% of the total outstanding liabilities. The majority of this balance consists of $105,135 of unfunded annual leave and the Federal Employees Compensation Act liability. The other unfunded liabilities include the GSA Tenant Improvement liability of $26,051; contingent liabilities of $15,679 and environmental clean up liabilities of $5,466. The balance of the environmental clean up costs reported in FY2002 included both environmental clean up and continent liabilities for equipment removal. During FY2003, the environmental costs were adjusted to reflect only those sites identified with hazardous waste. The remaining sites where only clean up of equipment remains to be completed were reclassified as contingent liabilities.

Financing Sources

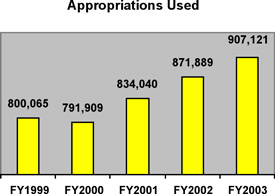

The majority of the USGS financing sources consist of net appropriations of $919,273; consisting of $925,287 from the surveys, investigations, and research appropriations, less rescissions of $6,014. Additionally, the Bureau is reporting imputed financing from costs absorbed by others of $56,237. The ending FY2003 financing sources were $251,182, or 21%, less than the $1,215,891 September 31, 2002 ending balance. The 2002 financing sources include a one time transfers in of $257,684 for a satellite donated from NASA. The FY2003 appropriations used totaled $907,121. Appropriations used have generally increased over the last five years. The amount of appropriations used represents financing sources USGS has available through Congressional appropriations. Appropriations are recognized as an accrual based financing source when the related expenses are incurred or assets are acquired.

The majority of the USGS financing sources consist of net appropriations of $919,273; consisting of $925,287 from the surveys, investigations, and research appropriations, less rescissions of $6,014. Additionally, the Bureau is reporting imputed financing from costs absorbed by others of $56,237. The ending FY2003 financing sources were $251,182, or 21%, less than the $1,215,891 September 31, 2002 ending balance. The 2002 financing sources include a one time transfers in of $257,684 for a satellite donated from NASA. The FY2003 appropriations used totaled $907,121. Appropriations used have generally increased over the last five years. The amount of appropriations used represents financing sources USGS has available through Congressional appropriations. Appropriations are recognized as an accrual based financing source when the related expenses are incurred or assets are acquired.

Budgetary Resources

The USGS received approximately 61%, or $919,973, of its total budgetary resources of $1,498,220 through net appropriations. Other major sources of budgetary resources include unobligated balances carried over from FY2002 and spending authority from offsetting collections, totaling $127,337 and $445,551, respectively. Of the total budgetary resources $1,342,739 were obligated as of September 30, 2003.

The majority of the budgetary resources were used during the current year to support surveys, investigations and scientific research. The FY2003 appropriations received includes; $64,434 in funds available only for cooperation with states and municipalities for water resource investigations; $15,398 to remain available until expended for conducting inquires into the economic conditions affecting mining and materials processing industries; $7,948 to remain available for satellite operations until expended; $24,463 for operation and maintenance of facilities and deferred maintenance and shall be available until September 30, 2004; $169,815 for biological research activity and the operation of Cooperative Research Units until September 30, 2004.

The offsetting collections from the Bureau's reimbursable program include the following: reimbursements from non-Federal sources are from States, Tribes, and municipalities for cooperative efforts and proceeds from sale to the public of copies of photographs and records; proceeds from sale of personal property; reimbursements for permits and licenses of the Federal Energy Regulatory Commission, and reimbursements from foreign countries and international organizations for technical assistance. Reimbursements from other federal agencies are for mission related work performed at the request of the financing agency.

The USGS also maintains a working capital fund that makes up 8% or $117,086 of the total budgetary resources. The fund established in November 5, 1990, is primarily used to invest funds from appropriations and reimbursable agreements without fiscal year limitation to purchase materials, supplies and equipment for long-term capital investments. The WCF also provides fee for service operations primarily for the Water Quality Lab and the Hydraulic Instrumentation Facility. The WCF allows the USGS to provide more efficient financial management of its telecommunications investments; acquisition, replacement, and enhancement of scientific equipment; facilities and laboratory operations, modernization and equipment replacement; drilling and training services; and publications.

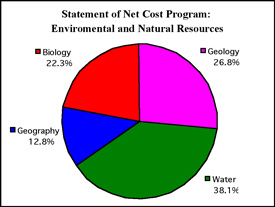

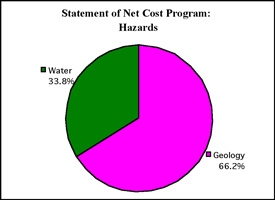

Composition of Net Costs

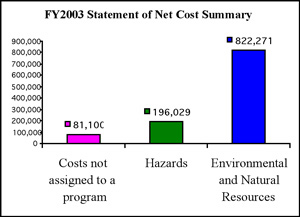

In FY2003, net cost of operations totaled approximately $1,099. In terms of net cost of operations supporting its two strategic goals, USGS spent 75% of the total to achieve its strategic goal of ensuring the continued availability of long-term environmental and natural resource information and systematic analysis and investigations; and 18% to ensure the continued transfer of hazards-related data, risk assessments, and disaster scenarios needed by our customers before, during, and after natural disasters. Costs not assigned to a program accounted for 7% of total net cost. The USGS organizational support of its strategic goals is provided by four discipline areas; Water, Geology, Mapping and Biology. The charts below will show net costs for each discipline by strategic goal.

Limitations to the Financial Statements

The consolidated financial statements have been presented to report the financial position and results of operations of the United States Geological Survey (USGS), consistent with the requirements of the Chief Financial Officers' Act of 1990. While the statements have been prepared from the books and records of USGS in accordance with generally accepted accounting principles for Federal entities and the formats prescribed by the Office of Management and Budget, the statements are in addition to the financial reports used to monitor and control budgetary resources which are prepared from the same books and records. The financial statements should be read with the realization that they are for a component of the United States government, a sovereign entity. Liabilities not covered by budgetary resources cannot be liquidated without the enactment of an appropriation, and the payment of all liabilities, other than for contracts, can be abrogated by the sovereign entity.

U.S. Department of the Interior, U.S. Geological Survey

URL: http://pubsdata.usgs.gov/pubs/03financial/html/analysis.html

Maintained by Eastern Publications Group

Last modified: 16:28:36 Tue 22 Nov 2016

Privacy statement | General disclaimer | Accessibility