Quantifying Potential Effects of China’s Gallium and Germanium Export Restrictions on the U.S. Economy

Links

- Document: Report (2.77 MB pdf) , HTML , XML

- Download citation as: RIS | Dublin Core

Acknowledgments

At the time of publication, detailed input-output tables for 2021 were not publicly available from the Bureau of Economic Analysis. The authors would like to thank Joshua Coyan, Michael George, Daniel Hayba, and Steve Textoris at the U.S. Geological Survey for reviews and feedback.

Abstract

China’s export controls on gallium and germanium exemplify concerns regarding the reliability of supplies of mineral commodities that are essential to economic development, national security, and transition to renewable energy. This report presents a new model that quantifies the potential effects of mineral commodity supply disruptions on the U.S. economy. After calculating postdisruption equilibrium prices and quantities, a nonlinear optimization routine was used along with economic input-output tables to estimate the effects of varying Chinese net export restrictions of gallium and germanium on U.S. gross domestic product (GDP). The results indicated that a complete restriction of China’s net exports of gallium and germanium could cause the U.S. GDP to decrease by $3.1 billion (with lower and upper estimates of $1.7 billion to $8.2 billion) and $0.4 billion ($0.01 billion to $1.1 billion), respectively, if disrupted separately, and $3.4 billion ($1.7 billion to $9.0 billion) if disrupted simultaneously. The proposed model can be applied to other commodities and disruption scenarios.

Plain Language Summary

China’s export controls on gallium and germanium illustrate concerns about the reliability of supplies of mineral commodities that are essential to economic development, national security, and transitioning to renewable energy. The U.S. Geological Survey created a new model to quantify the potential effects of mineral commodity supply disruptions from Chinese net export restrictions of gallium and germanium on U.S. gross domestic product (GDP). The results indicated that a complete restriction of China’s net exports of gallium and germanium could cause the U.S. GDP to decrease by $3.1 billion (with lower and upper estimates of $1.7 billion to $8.2 billion) and $0.4 billion ($0.01 billion to $1.1 billion), respectively, if disrupted separately, and $3.4 billion ($1.7 billion to $9.0 billion) if disrupted simultaneously. The proposed model can be applied to other commodities and disruption scenarios.

Introduction

Reliable supplies of mineral commodities are essential to the functioning of an interconnected global economy. Yet in the past several years, mineral commodity supply chains have faced considerable strain from the COVID–19 pandemic (Jowitt, 2020), the Russia-Ukraine conflict (Khurshid and others, 2023), as well as trade tensions among the world’s leading industrial nations (Gulley and others, 2018; Kalantzakos, 2020). These strains come at a time when demand for certain mineral commodities may grow considerably with the transition to renewable energy sources, increased urbanization, and the accelerating adoption of various technologies, including artificial intelligence, fifth-generation (5G) wireless cellular technology, and autonomous vehicles, among others (Nassar, 2023). Recent actions by the government of the People’s Republic of China to impose export controls on various gallium and germanium products (Ministry of Commerce and General Administration of Customs [China], 2023)—metals, compounds, and wafers that are used in certain integrated circuits, diodes, infrared lenses, and fiber optic cables that have become increasingly essential for consumer electronics, lighting and displays, telecommunication networks, and defense applications—exemplify concerns among import-dependent nations regarding the reliability of supplies of mineral commodities that are necessary for their economic development and national security.

To help identify the mineral commodities of most concern, governmental agencies, academic researchers, and multinational corporations have developed different criticality assessments (National Research Council, 2008; Graedel and others, 2015; Ku and others, 2018; Nassar and others, 2020a; Schrijvers and others, 2020; Nassar and Fortier, 2021; Bauer and others, 2023; Grohol and Veeh, 2023). These analyses typically utilize various combinations of indicators to assess the risks. Although the scopes, methodologies, and metrics used in these assessments vary, their outcome is generally similar: a (prioritized) matrix or list of commodities of greatest concern to the nation, region, company, sector, or technology in question. These assessments are generally relatively simple by necessity because they attempt to assess supply chains of numerous commodities, many of which have very limited data. Moreover, previous analyses do not assess supply risks using standard economic terms (for example, lost economic activity or jobs lost), thereby limiting their usefulness as well as their comparability to other risks or the costs of mitigation strategies.

In contrast, Manley and others (2022a) extended a methodology originally developed by Levine and Yabroff (1975) to assess the economic effects of mineral commodity supply disruptions. That methodology used economic input-output (IO) tables and a linear programming routine to determine the economic effects on individual industries, sectors, and the entire economy at different levels of mineral commodity supply disruption. Specifically, the objective function of the model sought to maximize U.S. gross domestic product (GDP) subject to a set of constraints that included a mineral commodity availability constraint that pertained to the disruption scenario, a production capacity constraint that simulated the availability of excess production capacity of each industry, and a minimum final demand constraint that indicated the lowest acceptable level of demand by final uses (personal consumption expenditure; private fixed investment expenditures; changes in private inventories; net exports; and Federal, State, and local consumption and investment expenditures) required of each industry. The terminology used in the methodology is defined in the U.S. Bureau of Economic Analysis (BEA) IO handbook (Horowitz and Planting, 2006). A key benefit of that model is that it does not require much additional data beyond the IO tables and the mineral commodity consumption of each domestic industry. With the best available information on mineral commodity consumption, Manley and others (2022a) were able to apply the methodology to 56 mineral commodities, with a follow-up analysis on the automotive and electronics industries (Manley and others, 2022b).

In addition to using outdated [2012] data due to the lack of more recent detailed IO tables from the BEA, the methodology presented by Manley and others (2022a) has several limitations beyond those generally attributable to IO frameworks, namely fixed industry structure and constant returns to scale. First, the results in absolute terms are strongly dependent (as shown by Levine and Yabroff [1975] and Manley and others [2022a]) on a largely arbitrary selection of the level of minimum final demand for each industry. Second, the model depends on the assumption that all industry output is homogeneous. Third, the model does not account for changes in mineral commodity prices due to the supply disruption or the absolute level of consumption of the mineral commodity.

The first limitation stems from the fact that Leontief IO models (Leontief, 1951) are demand-driven, meaning that final demand determines how much output is needed from each industry. Final demand must, therefore, be provided exogenously to the model. As such, modeling an exogenous supply disruption needs to be translated into an exogenous demand shock that is then supposed to endogenously determine industry output levels. As explained by Oosterhaven (2017), this circular reasoning is present in so-called inoperability input-output models, which have become widely used in the field of risk and disaster assessments. A supply-driven counterpart to the Leontief IO model was developed in 1958 by Ghosh (1958) to examine planned economies. However, due to a variety of reasons, that model could yield unrealistic results (Oosterhaven, 1988).

The second limitation—industry output (and input) homogeneity—is an assumption inherent in all IO frameworks. An industry may produce several different types of outputs, each with different material compositions. In the model presented by Manley and others (2022a), when the consumption of a specific mineral commodity is linked to an industry, via the mineral commodity availability constraint, the entire output of that industry is assumed to utilize that mineral commodity. This may be a reasonable assumption for certain mineral commodities that may be used in virtually all products of a given industry (for example, copper is used in the manufacturing of all electronics). However, this is an issue for minor elements, such as gallium and germanium, which are typically used in specialized applications that may represent only a small fraction of an industry’s output.

Thirdly, by not accounting for the absolute value of the mineral commodity consumed, the model presented by Manley and others (2022a) could yield the same results for two mineral commodities if they were consumed in the same relative proportions by the same industries even if their consumption levels were vastly different. Similarly, that model does not account for differences in mineral commodity prices, nor does it account for changes to those prices due to the supply disruptions.

The model detailed in this report addressed each of these shortcomings; the details are presented in the “Materials and Methods” section of this report. The new model was applied to the production, consumption, and supply chains of gallium and germanium under different scenarios of individual and simultaneous disruption of China’s net exports.

Background on Gallium and Germanium

There are several aspects of the supply and demand of gallium and germanium that make their supply chains particularly susceptible to disruption. Similar to the production of many mineral commodities, the primary production of gallium and germanium is highly concentrated in a single country, namely China (Nassar and others, 2020b). Since 2014, more than 90 percent of primary gallium has been produced in China, with the remainder coming from Japan, Russia, South Korea, and Ukraine (app. 1; Jaskula, 2010–23; U.S. Geological Survey, 2024) Additional production capacity outside of China and these currently producing nations is reportedly available in Germany, Hungary, and Kazakhstan (app. 1; Jaskula, 2010–23; U.S. Geological Survey, 2024), although the ability of this capacity to be immediately available is not clear. China is also the world’s leading producer of primary germanium, with Canada, Belgium, and Russia providing the remainder (Guberman, 2010–16; Guberman and Thomas, 2017; Thomas, 2018–23; U.S. Geological Survey, 2024). Moreover, gallium and germanium are two of a number of mineral commodities for which production is currently only economical as a byproduct during the extraction of other mineral commodities (Nassar and others, 2015). Specifically, gallium is most commonly recovered by ion exchange from the sodium aluminate Bayer liquor during the processing of bauxite ores and, to a much lesser extent, from the residues generated during the leaching of zinc oxide that is obtained from roasting sphalerite ores (Project Blue Group Ltd., 2023). Germanium is also recovered during the leaching of certain zinc smelter residues and from coal ash. These factors suggest that the supply of gallium and germanium may be price inelastic (Nassar and others, 2015), but there has been no quantitative assessment of that elasticity previously.

On the demand side, as a group III element, gallium is combined with group V elements to form a group of semiconductor materials that are known as III–V compound semiconductors (for example, aluminum gallium arsenide [AlGaAs], gallium arsenide [GaAs], gallium nitride [GaN], indium phosphide [InP], indium arsenide [InAs], and indium antimonide [InSb]). Whether as a substrate or as an epitaxial layer that is grown on a substrate (for example, GaN on silicon, sapphire, silicon carbide, or GaAs), gallium-based semiconductors find use predominately in radio frequency electronics (for example, radio frequency power amplifiers for mobile handsets and wireless area networks), power electronics (for example, direct current to direct current [DC–DC] converters, onboard chargers, and traction inverters in electric vehicles), photonics (for example, vertical-cavity surface-emitting lasers for proximity sensors and edge-emitting lasers for automotive light detection and ranging [lidar] applications), light-emitting diodes (LEDs) for lighting and displays, as well as high-efficiency solar cells, mainly in space solar photovoltaic (PV) cells (Yole Développement, 2018, 202051). Gallium is also used in copper indium gallium (di)selinide (CIGS) thin-film PV cells and as a dopant in the industry-dominant crystalline silicon PV cells where it has recently been replacing boron to provide extended lifetimes and reduced degradation of performance over time (Feldman and others, 2024). In China, gallium has been used as an additive in neodymium iron boron permanent magnets (Løvik and others, 2015; Project Blue Group Ltd., 2023). In addition to being the main substrate for the III–V high-efficiency space solar PV cells, germanium is also used in semiconductor applications (for example, silicon germanium [SiGe], IV–IV compound semiconductor). However, germanium finds its main use as a dopant to increase the refractive index of the core of optical fibers and as a material for infrared lenses and windows, applications that have important uses in telecommunications and defense, respectively. Details regarding these and other uses are listed in appendix 1.

Although there are substitute materials (for example, silicon-based semiconductors), gallium and germanium products have specific properties (for example, high electron mobility for gallium and high refractive index for germanium) that make them uniquely suited for certain applications. For example, with faster switching speed and higher breakdown voltage, GaN power devices outperform traditional silicon-based devices, making them ideal in certain applications such as DC–DC converters in electric vehicles that require high power density and energy efficiency, to allow for longer driving ranges, lighter batteries, better thermal management, and lower cost (Prajapati and Balamurugan, 2023). As such, substitution may be limited. In addition to the lack of quantitative estimates of price elasticities of demand, the markets for gallium and germanium are small and their production, trade, and consumption are opaque. All these factors contribute to making the market assessment especially challenging and full of uncertainties.

Materials and Methods

The model in this report is conceptually similar to what has been proposed by Oosterhaven and Bouwmeester (2016) and Li and others (2022). Specifically, the assumption behind those models is that, in the short run after a disruption event, economic actors (including industries, consumers, and governments) are expected to attempt to continue or re-establish predisruption economic activity patterns as closely as possible (Oosterhaven and Bouwmeester, 2016). The proposed model used an optimization routine with an objective function (eq. 1) that seeks to minimize the differences between predisruption and postdisruption economic activity, as follows:

wherez and z’

are the predisruption and postdisruption intermediate demand, respectively;

y and y’

are the predisruption and postdisruption final demand, respectively;

v and v’

are the predisruption and postdisruption value added, respectively; and

i, j

are subscripts that indicate individual industries.

Data for each of the predisruption parameters of equation 1 were available for the United States from the BEA at the detailed 405-industry group level every 5 years to correspond with the U.S. economic census. The BEA publishes updates for the interim years but only at aggregated levels (Bureau of Economic Analysis, 2023). These aggregated data are based on estimated detailed IO tables (BEA, written comm., June 26, 2023). The most recent data provided [2021] were used in this report.

The decision variables in the model were each industry’s output (x′) or similarly the change in industry output from their initial values. The optimization was subjected to several constraints, one of which was a mineral commodity availability constraint, as follows:

This constraint specifies that the total amount of the mineral commodity used by domestic industries in the United States—calculated as the product of the new (postdisruption) output of a consuming industry and the mineral consumption ratio (m) of that industry, summed across all industries—must be less than or equal to the total quantity of the mineral commodity (M′) that is available under the specified disruption scenario. To simulate a disruption of multiple mineral commodities simultaneously (for example, gallium and germanium together), an additional mineral commodity availability constraint (eq. 2) can be added. The consumption of each mineral commodity was linked to an individual industry, as defined by the BEA IO tables (app. 1).Nominally, the material consumption ratio (m) in equation 2 is calculated by dividing the mineral commodity consumption of that industry by the initial (that is, predisruption) output of that industry. However, as indicated in the “Introduction” section of this report, this method can be problematic in cases where only a small portion of the industry’s output uses the mineral commodity. One approach to address this industry homogeneity issue is to expand the IO tables to add rows and columns that are specifically linked to the mineral commodity in question. For example, a consuming industry could be split into two industries: one that uses the mineral commodity in question and another that does not. This approach requires substantial amounts of additional data and thus undermines a key benefit of using IO models—readily available tables. Instead, an alternative approach was employed in this report that requires only one additional piece of information: how much of an industry’s output used the commodity in question. To do this, the material consumption ratio (m) was defined as a function of an industry’s output, as follows:

Using this approach, a material consumption ratio’s value decreased to zero if the postdisruption industry’s output decreased to or below the level for which the remaining output of that industry did not use the mineral commodity in question. For example, if only 10 percent of an industry’s output used the mineral commodity in question, then a threshold level (τ) was set at 10 percent, and the material consumption ratio dropped to zero if the industry’s output decreased by 10 percent or more (decreased to or below 90 percent of its original value). Data regarding the threshold level τ for each industry-mineral commodity combination were estimated using data from the U.S. Census Bureau (2022, 2023) or market research reports (app. 1).

Unlike a strict constraint, this approach allowed the model to decrease a consuming industry’s postdisruption output level below the threshold, but declining below that output level did not further affect how much of the mineral commodity was directly consumed because the material consumption ratio became zero. The rationale behind this approach is that the industry’s output that will be affected first is that which is the direct consumer of the mineral commodity. Any further decreases in the industry’s output would be due to secondary effects associated with interindustry demand. This approach may not work well if the mineral commodity-containing part of the industry’s output is purchased in notably different proportions by the downstream industries as compared to the overall output of the industry. In such cases, IO table expansion would be the better option.

When modeling the simultaneous disruption of two commodities that are used by the same industry (for example, gallium and germanium in semiconductors), another decision variable (θ) was introduced in the model, which determined the percent (bounded from 0 to 100 percent) of that industry’s output decrease that was using the first commodity, denoted with subscript , with the remainder of the output decrease (1−θ) for the second commodity, denoted with subscript b, as follows:

This approach assumes there were no overlapping or concurrent uses in the industry’s output (the commodities are used in different applications that are produced by the same industry). If there is complete overlap (the commodities are only used in the same applications), then the use of θ was unnecessary. In the case of gallium and germanium, although both are used in similar semiconductor applications (for example, radio frequency power amplifiers and photonics), they were assumed to only be used concurrently in III–V high-efficiency solar cells (where germanium was used as the substrate for the growth of GaAs). Given that high-efficiency solar cells represent a very small percentage (likely less than 0.1 percent) of the U.S. semiconductor and related devices industry’s output, this concurrent use was disregarded in the model. Because of this assumption, the results may be slightly overestimated.The quantity of the mineral commodity that was available after the disruption was based on the initial quantity consumed (M) and the relative shift in supply to the new equilibrium quantity (n′):

The relative shift in supply to the new equilibrium quantity was determined by the exogenously provided disruption scenario less any releases of available inventories, any excess production capacity outside of China (κ), the mineral commodity’s price elasticity of supply (εS), and its price elasticity of demand (εD). Specifically, the exogenously provided supply disruption scenario (a decrease in China’s net exports of gallium or germanium) shifts the supply curve to the left by a specific quantity, which is partially or completely offset by any releases from inventories held by governments, producers, or consumers. This inventory-adjusted shift in quantity (ΔQs) or relative shift in quantity (, where Qs is the initial equilibrium quantity that was based on a calculated apparent consumption) along with the price elasticities were used to determine the new equilibrium price (P′) relative to the initial price (P), as follows: With the new equilibrium price, the relative change to the new equilibrium quantity (n′) was determined:Following the approach outlined by Shojaeddini and others (2024), the price elasticities were estimated empirically using a two-stage least-squares and instrumental variable approach for panel data. For time series data, an autoregressive distributed lag model was used instead. Details regarding the approaches and the estimations are provided in appendix 1. In general, the demand for a mineral commodity with limited substitutability would be less price elastic and would thus witness a larger price increase during a supply disruption than a mineral commodity with several suitable substitutes. Similarly, a mineral commodity with a constrained ability to increase the quantity supplied would witness a larger price increase than a commodity for which the quantity supplied can be readily expanded.

If the scenario provided a shift in supply that was large enough to allow all available excess production capacity to be used (meaning that the demand curve intercepts the vertical portion of the supply curve), then equations 7 and 8 become:

Note that these equations are for a short-term disruption (nominally, up to 1 year), such that there was no shift in the demand. The full derivation of these equations, including the possibility of a demand curve shift, is provided in appendix 1.Given that this analysis was specific to China imposing export controls, the data were divided into two regions—China and the rest of the world—and then, for each mineral commodity, the new equilibrium price and quantity for the rest of the world were determined based on China’s net exports of the mineral commodity to the rest of the world, the excess production capacity of the mineral commodity in the rest of the world, and the predisruption apparent consumption of the mineral commodity in the rest of the world. The quantity that would be available to the United States was assumed to decrease proportionally with that of the rest of the world.

The next constraint used in the model was an industry production capacity constraint, which stipulated that the output of each industry cannot be negative nor exceed that of its capacity ():

The output capacity of an industry was calculated by dividing its predisruption output level by its capacity utilization rate. The Board of Governors of the Federal Reserve System publishes monthly capacity utilization data for the manufacturing sector in the United States (Board of Governors of the Federal Reserve System, 2023) These data are generally available at the three-digit North America Industry Classification System (NAICS) subsector level or equivalent, and in a few cases, at the four-digit NAICS industry group level. In contrast, the BEA IO tables are generally reported at the four-, five-, or six-digit NAICS level equivalent. As such, the capacity utilization data at the three- and four-digit levels were applied to the most appropriate level or sublevel, accordingly. For the remaining industries outside the manufacturing sector, the capacity utilization rate was set to 1, meaning the predisruption industry output level was set as the maximum for industries for which production capacity utilization data were not available.To account for the limited availability of labor and capital, a constraint was set on the GDP such that its postdisruption value cannot exceed the potential GDP (GDPPotential), as estimated by the Congressional Budget Office (2024), as follows:

Generally, this would not be a binding constraint for supply disruptions scenarios but may play a role if the outputs of certain domestic industries grow markedly. The next constraint provided the supply and demand equilibrium, using the Leontief equation, as follows: where I is the identity matrix, A is the 405-by-405, industry-by-industry direct requirements matrix, and as previously defined, x and y are the industry output and final demand, respectively. For these variables, data provided by the BEA were used (BEA, written comm., June 26, 2023). Values for individual interindustry intermediate demand (z) were calculated using the direct requirements matrix:Additionally, price effects were taken into account by adjusting the profitability of the consuming industries. Specifically, the increased price of the mineral commodity decreased the gross operating surplus of a consuming industry—a component of its value added as follows:

As indicated in equation 15, how much each industry’s value added decreased depended on two factors: how much the mineral commodity’s price increased and how much the industry’s output decreased. The latter affected both the decrease in value added directly as well as through how much of the mineral commodity the industry consumed relative to what it previously consumed. This allowed the price and quantity effects to be determined separately in the calculation of value added. Because postdisruption industry output was determined endogenously in the model, the influence of the price effect on an individual industry’s value added was determined dynamically by the model.

Note that the approach of incorporating the price effects into the value-added component (eq. 15) implicitly assumed that the industries that are the initial or direct consumers of the mineral commodity absorbed the entire price increase, with none of the price increase being passed on to downstream industries or final consumers. This is not completely realistic in all cases but may be a reasonable assumption in the short term. Also note that the change in the mineral commodity’s price was accounted for in the calculation of value added but not in the constraint on GDPPotential (eq. 12). The price effect was also deliberately not translated into the other variables (for example, industry output or output to final demand or intermediate demand) to maintain price equilibrium throughout the IO model while still accounting for the change in the prices of mineral commodities in estimating the decrease in GDP.

The United States is not a producer of primary gallium or germanium products. If it were, under this specific set of scenarios, the domestic primary production of the mineral commodity (R) would be expected to increase and domestic producers would benefit from both the increased output and the increased price of the mineral commodity that they produce. Just as the decrease in mineral commodity available in the United States was assumed to decrease proportionally to that of the rest of the world, domestic production could be assumed to grow proportionally to that of the rest of the world based on the new equilibrium quantity up to its reported production capacity (Rcap). Therefore, a constraint could be established such that domestic mineral commodity production increases accordingly:

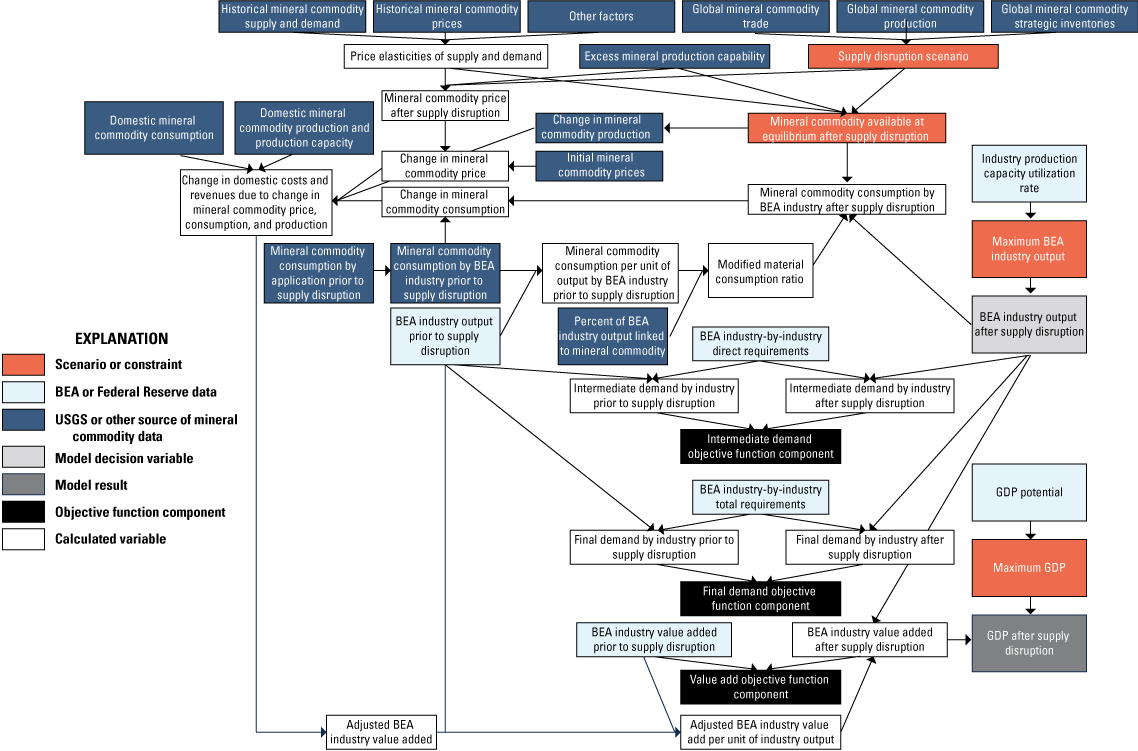

where p′ is the growth rate in the predisrupted production (as determined by the new equilibrium quantity relative to predisruption production) and r is the ratio of production of a mineral commodity to the industry output. This mineral commodity production ratio is similar to the mineral commodity consumption ratio in that it accounts for the fact that the production value of each mineral commodity accounts for only a fraction of an industry’s output. The mineral production ratio can thus be calculated as follows: where φ is the threshold level, which could be estimated by multiplying the quantity of domestic production of the mineral commodity in question by its price and dividing it by the producing industry’s predisruption output. The increased production level and higher price of the domestic mineral production industry (typically under the BEA sector for mining [212] or refining and smelting [331]; Bureau of Economic Analysis, 2023) translates into higher gross operating surplus, which can be accounted for in the producing industry’s value added, as follows: The proposed model for a single commodity disruption is presented diagrammatically in figure 1.

Diagram of a model for quantifying potential effects of mineral commodity supply disruptions on the U.S. economy. The diagram depicts the different data, constraints, and variables used in the model, as well as their sources and how they are interlinked. Bureau of Economic Analysis (BEA) data are from Bureau of Economic Analysis (2023); Federal Reserve data are from Board of Governors of the Federal Reserve System (2023). U.S. Geological Survey (USGS) data are from U.S. Geological Survey (undated). GDP, gross domestic product.

Data regarding mineral commodity production, production capacity, trade, inventories, and consumption for China, the United States, and the rest of the world were collected from a variety of sources (app. 1). All data pertain to 2021 or 2022, the latest years for which a complete set of IO tables and mineral commodity data were available before China’s export controls were established.

Given the lack of transparency in the gallium and germanium markets, a sensitivity analysis was performed in which each of the key parameters used in the model was varied to provide cases labeled as “low impact” and “high impact” in addition to the baseline case (app. 1). Finally, given that it is currently [2024] unclear how much (if any) of China’s net exports of gallium and germanium products will ultimately be restricted, the level of restriction was varied from 10 to 100 percent.

Results and Discussion

The price elasticities of demand for gallium and germanium were estimated to be −0.53 and −0.245, respectively. Meanwhile, the price elasticities of supply in the short run for gallium and germanium were estimated to be 0.40 and 0.69, respectively (app. 1). These elasticities suggest that the supply and demand for gallium and germanium were price inelastic, with absolute values falling between 0 and 1. The supply of germanium exhibited greater price elasticity compared with that of gallium, whereas the price elasticity of demand for germanium was lower (in absolute value) than that for gallium. It is important to highlight that the price elasticity of demand for gallium was derived from panel data within a static framework, potentially resulting in a larger absolute value compared to the short-run elasticity. In contrast, the price elasticity of demand for germanium was based on time-series data (app. 1), with the reported numbers reflecting short-run elasticity.

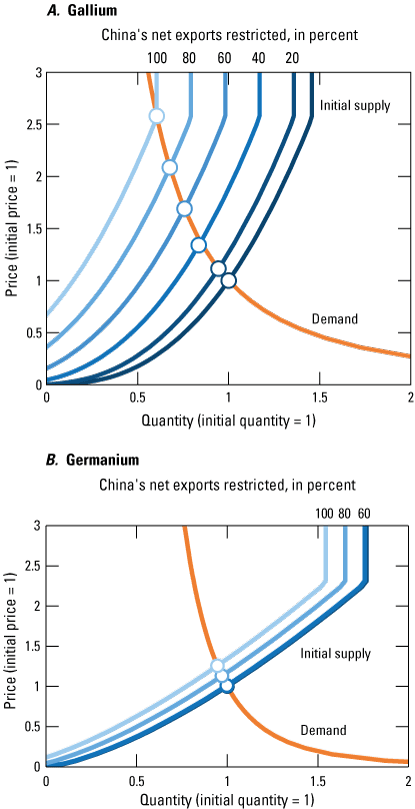

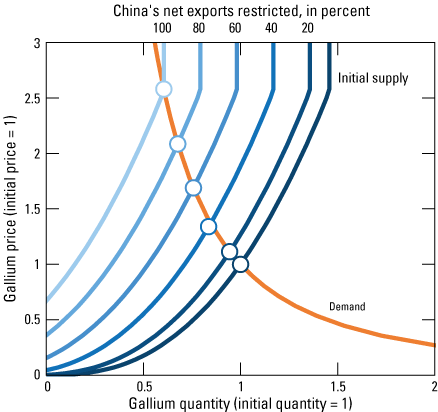

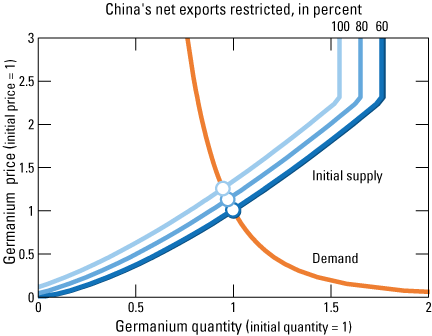

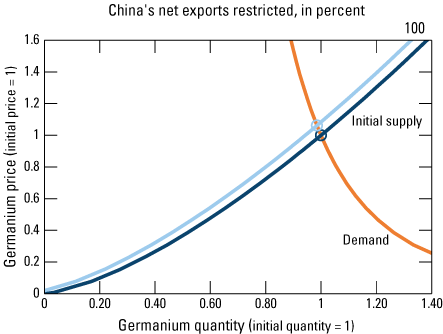

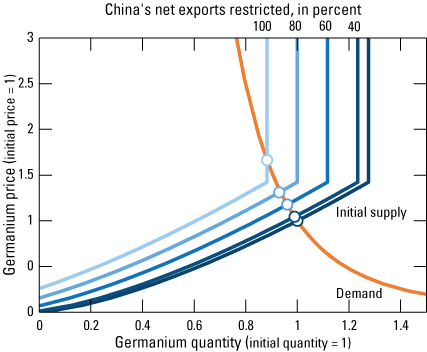

These price elasticities, along with data on China’s net exports and the rest of the world’s (excluding China) production, production capacity, consumption, and inventories, were used to estimate new equilibrium prices and quantities for the rest of the world under several different levels of supply disruption (as defined by the percentage of China’s net exports that were restricted). The results are displayed in figure 2.

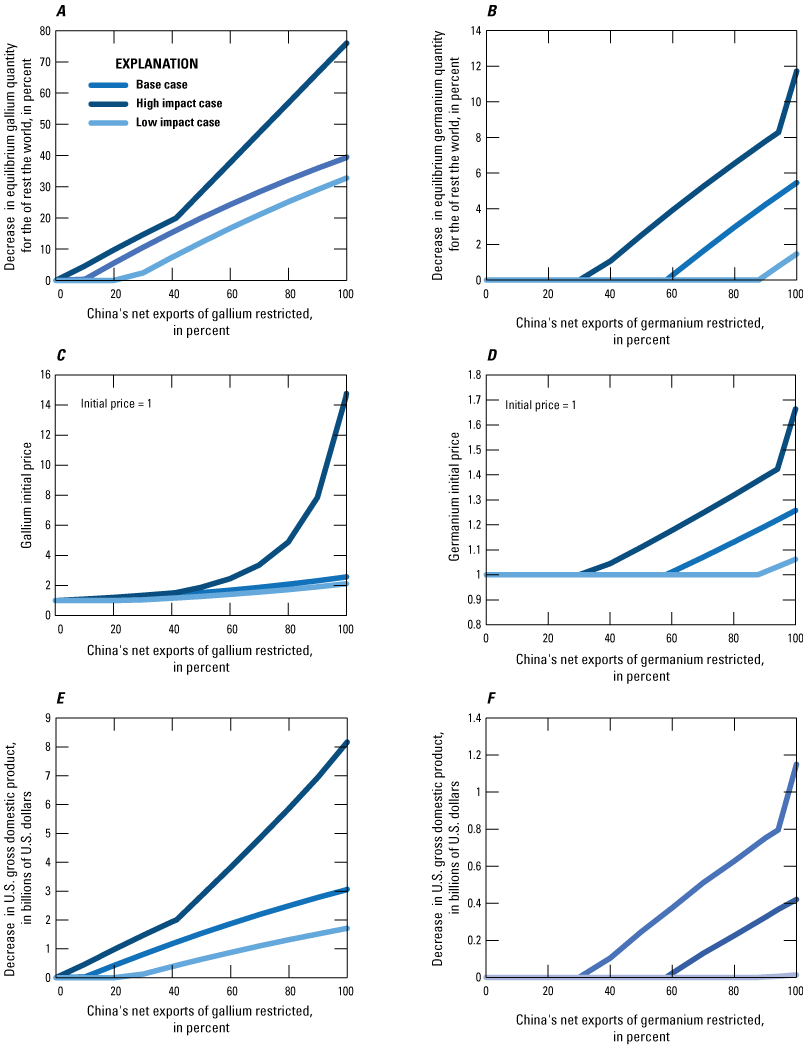

Estimated equilibrium quantities and prices for the rest of the world under different scenarios of Chinese net export restriction of A, gallium and B, germanium.

The results indicated that a complete restriction of China’s net exports of gallium, which were estimated to be 159 metric tons (t) out of a total world production of 638 t in 2022 (fig. 1.1; table 1.10), would cause gallium prices in the rest of the world to increase by more than 2.5-fold, while the quantity of gallium available to the rest of the world would decrease by about 39.5 percent. In contrast, a complete disruption of China’s net exports of germanium, which were estimated to be 35 t out of a total world production of 210 t in 2022 (tables 1.14 and 1.17), would cause germanium prices to increase by 26 percent and the quantity available to the rest of the world to decrease by about 5.5 percent. Less than complete restrictions of China’s net exports would result in correspondingly lower price increases and quantity decreases (fig. 2; app. 1). A complete restriction of China’s net exports of germanium has a lower effect than that of gallium due to the differences in price elasticities and the higher levels of germanium production, production capacity, and inventories in the rest of the world. Restriction of as much as 58 percent of China’s net exports of germanium could be offset by available inventories, thereby resulting in no shift in the supply curve.

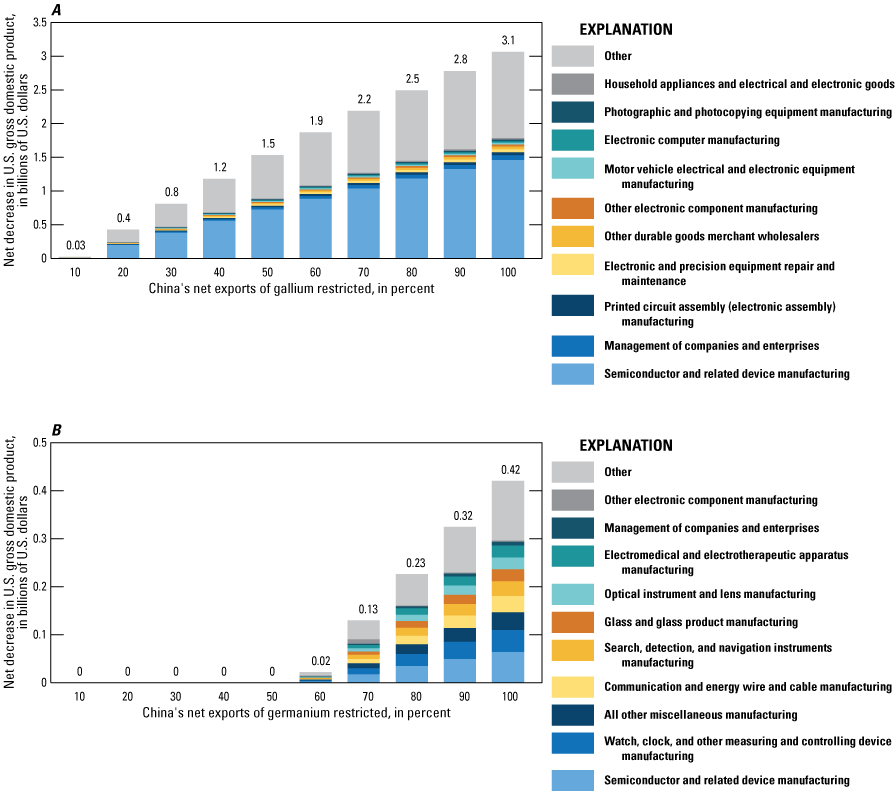

The effects on the U.S. GDP at the level of individual industries and the economy overall were calculated using these relative shifts in quantities and prices in the IO model. The results (fig. 3) indicate that the U.S. GDP would decrease by $3.1 billion (or about 0.013 percent of U.S. GDP in 2021) if all of China’s net exports of gallium were restricted for an entire year. Nearly half (46.5 percent) of the decrease would come from the semiconductor and related device manufacturing industry (BEA industry code 334413)—the industry to which gallium consumption was directly linked to in the model. The remaining decrease would come from a wide assortment of industries, including several that are downstream from the 334413 industry, namely the printed circuit assembly (electronic assembly) manufacturing (334418), motor vehicle electrical and electronic equipment manufacturing (336320), and electronic computer manufacturing (334111). Notably, aside from the 334413 industry, no other individual industry dominated the decrease in U.S. GDP, and each industry’s relative contributions to the decrease remained largely consistent at different levels of restriction.

Estimated net decrease in U.S. gross domestic product at different levels of restrictions of China’s net exports of A, gallium or B, germanium, by industry.

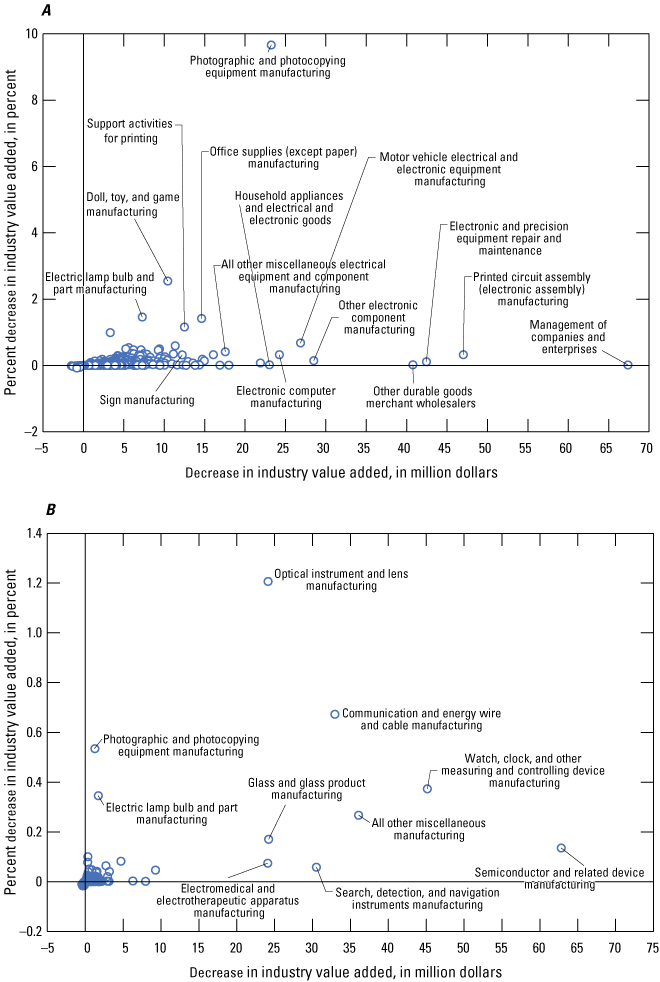

Scatterplots of absolute (horizonal axis) and relative (vertical axis) decrease of industry value added at 100 percent (%) restriction of China’s net exports of A, gallium and B, germanium. The semiconductor and related device manufacturing industry is not displayed in A due to horizonal axis truncation.

The decrease in U.S. GDP was estimated to be $0.4 billion under a scenario of complete restriction of China’s net exports of germanium. This was markedly lower than the decrease associated with the restriction of gallium primarily because the estimated decrease in equilibrium quantity was smaller, approximately 5.5 percent for germanium as compared to 39.5 percent for gallium. Therefore, excess production capacity and inventories in the rest of the world, which reduce the dependency on China, play an important role in reducing the effect of a germanium supply restriction.

Unlike the effect on the U.S. GDP from gallium restrictions, the effect on the U.S. GDP from germanium restrictions was not dominated by a single industry. Instead, the decrease was contributed to nearly evenly from several industries, with the largest contributions to the decrease coming from semiconductor and related device manufacturing (334413) and watch, clock, and other measuring and controlling device manufacturing (33451A; this is the industry that includes gamma-radiation detection equipment manufacturing that uses germanium). Although these were industries that were directly connected to germanium consumption in the model, they were not the largest direct consumers of germanium. The largest direct consumers of germanium were communication and energy wire and cable manufacturing (for fiber optic cables; 335920) and search, detection, and navigation instrument manufacturing (for infrared equipment; 334511). As before, restrictions of as much as 58 percent of China’s net exports of germanium were offset by available inventories.

Industries that contributed the most to the overall U.S. GDP decrease were not necessarily the industries that were most affected by the disruption. That is because some industries were larger contributors to GDP than others. The photographic and photocopying equipment manufacturing (333316) industry had the largest relative decrease in value added under a complete restriction of China’s net exports of gallium (fig. 4A). Other industries that had large relative decreases under this scenario were the doll, toy, and game manufacturing (339930), electric lamp bulb and part manufacturing (335110), and office supplies (except paper) manufacturing (339940) industries. For germanium (fig. 4B), the industry that had the largest relative decrease in value added was the optical instrument and lens manufacturing (333314). Again, this industry was not the largest consumer of germanium and did not have the largest absolute decrease in value added. Other industries that had large relative decreases in value added under this scenario were the communication and energy wire and cable manufacturing (335920), photographic and photocopying equipment manufacturing (333316), watch, clock, and other measuring and controlling device manufacturing (33451A), and electric lamp bulb and part manufacturing (335110) industries, all of which were directly linked to germanium consumption in the model.

Sensitivity Analysis

The results from the sensitivity analysis (fig. 5) illustrated the effects of varying key parameters (tables 1.10 and 1.26) on three results: changes in equilibrium quantities, prices, and U.S. GDP. Although not statistical confidence intervals, these results provide a window of likely ranges. For gallium, the results indicated that the decrease in U.S. GDP could be as high as $8.2 billion or as low as $1.7 billion. This relatively large range follows the change in equilibrium quantity but is somewhat more pronounced for the high-impact case at the highest levels of restrictions because of the notably higher prices and the higher percentage of the semiconductor and related device manufacturing industry that was assumed to use gallium. The lower and upper values of U.S. GDP decrease for germanium were estimated to be $0.01 billion and $1.1 billion, respectively. Again, these germanium results closely follow the change in equilibrium quantity.

Sensitivity analysis displaying the effects of restricting (from 0 to 100 percent [%]) China's net exports of gallium and germanium on the A and B, rest of the world postdisruption equilibrium quantities, C and D, rest of the world postdisruption equilibrium prices, and E and F, U.S. gross domestic product (GDP) for the baseline, low-, and high-impact cases.

The change in slope for both the decrease in equilibrium quantity and U.S. GDP for gallium in the high-impact case occurs at a restriction of just over 41 percent of China’s net export. This was the point where the shift in the supply curve was large enough such that all the available excess production capacity was used (app. 1). That was the point where the demand curve intercepted the vertical portion of the supply curve, which resulted in larger increases in both changes in equilibrium quantities and prices at net export restrictions beyond that point. There was also a change in the slope in the result for gallium in the baseline case at a disruption level of 99.8 percent of China’s net exports due to the same reason (fig. 5A). This change in slope, however, did not occur for gallium in the low-impact case because the supply shift was small and the inventories and excess capacities in the rest of the world were larger. The change in slope only occurred for germanium in the high-impact case at a restriction of 94.1 percent of China’s net exports.

Comparison of Price and Quantity Effect

As described in the “Materials and Methods” section of this report and illustrated in equation 15, the modeled decrease in U.S. GDP is the result of two factors: decrease in industry output (to meet the mineral commodity availability constraint) and increase in mineral commodity prices. Both effects played a role in the results, but their contributions were not equal. When the model was simulated for the complete restriction of China’s net exports, higher prices only contributed 6.1 percent of the decrease in U.S. GDP for gallium and 2.2 percent of the decrease in U.S. GDP for germanium. These percentages were slightly lower at lower levels of China’s net export restriction and reached no higher than 12 to 16 percent in the results of the sensitivity analysis. These results suggested that the decrease in quantity available had far more of an effect on the decrease of the U.S. GDP than the increased prices, which is as might be expected given that the value of gallium- and germanium-containing devices (in other words, the value of the output of the industries) is notably greater than the cost of gallium and germanium raw materials. This may not be the case for all commodities because the ratio of the value of the commodities and the products that they are used in can vary markedly. It would also be dependent on the specific scenario and the price elasticities.

Simultaneous Disruptions

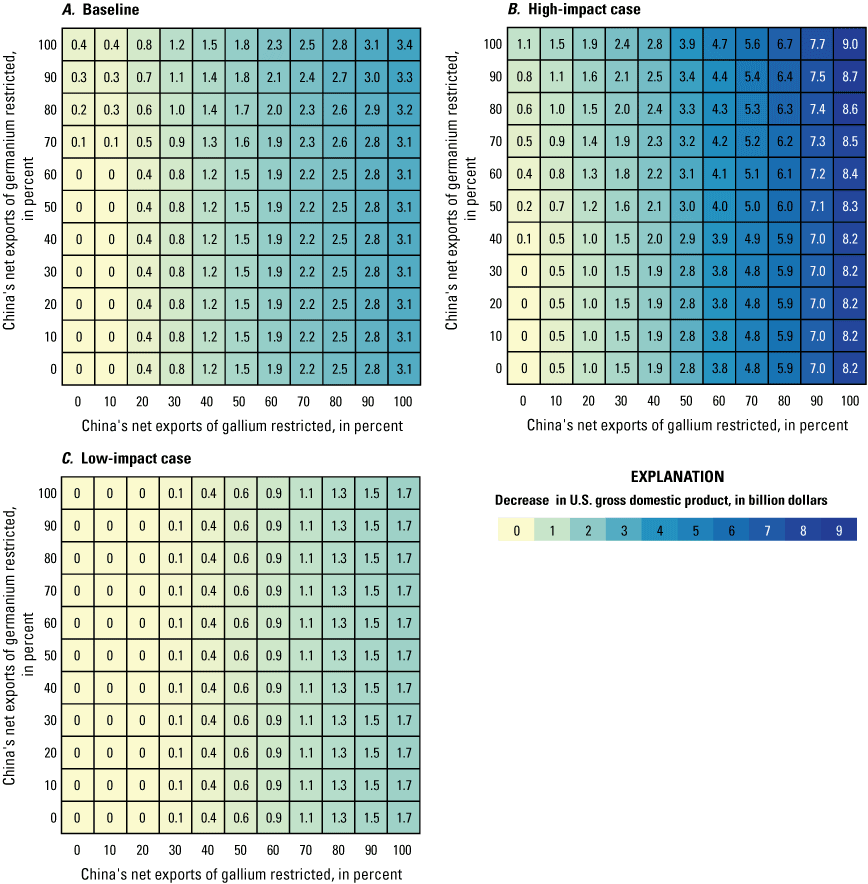

A complete and simultaneous restriction of China’s net exports of gallium and germanium was estimated to cause U.S. GDP to decrease by $3.4 billion ($1.7 billion to $9.0 billion for the low- and high-impact cases, respectively; fig. 6). The results from the simultaneous restrictions show the larger effect of gallium restrictions as compared to germanium restrictions. Furthermore, these decreases were slightly lower than the sum of the decreases from each mineral commodity when restricted individually. This was due to the interconnectedness of the affected industries (industries that would nominally be affected by the restriction of a commodity are also affected by the restriction of the other commodity and so their outputs do not decrease further). The effect on the U.S. GDP from the simultaneous disruption of both gallium and germanium would have been even lower than the sum of the effects from the restrictions on the individual commodities if some degree of concurrent uses among gallium and germanium were assumed. In contrast, one would expect the effect of simultaneous restrictions of mineral commodities that are used in notably distant sectors of the economy to have an effect that is closer to the sum of the effects of individual commodities.

Heat maps displaying the estimated effects of simultaneous restrictions of China’s net exports (from 0 to 100 percent [%]) of gallium and germanium on the U.S. gross domestic product (GDP) for the A, baseline, B, low-, and C, high-impact cases of the sensitivity analysis.

Limitations and Applicability

As with all models, there were various limitations and assumptions within this model that a reader should be cognizant of while interpreting the results. Although many of the uncertainties associated with the various assumptions were addressed via the sensitivity analysis, some were inherent to the model. For example, although the assessment of price elasticity of demand captured short-term substitution effects for gallium and germanium, the model did not account for substitution effects among downstream industries due to the rigid structure of the IO tables. For example, gallium and germanium are used in wireless telecommunication technologies and fiberoptic cables, which are potential substitutes for each other in certain instances. Although the model determined which industries consumed the postdisruption available gallium and germanium, it did not account for the possibility of downstream industries or final consumers switching between the two telecommunication options. This, however, might be an acceptable assumption in the short term as such changes likely require longer periods to occur. The model also did not account for the effects of changes in gallium or germanium prices on the prices of their substitutes and their associated consuming industries and assumed constant elasticities and shifts in the supply curves when calculating the new equilibriums.

Another simplifying assumption was that the different forms of gallium and germanium were interchangeable. That may not be the case as there may be limits to production capacities for certain forms (for example, reduction of an oxide to a metal or the production of high-purity single crystals). As discussed in the “Materials and Methods” section of this report, another limitation was that, even at the detailed level, the IO tables were not granular enough for some of the niche uses of these minor elements. The modified material consumption ratio addressed this issue by affecting only a portion of the consuming industry’s output. However, this approach implicitly assumed that the mix of downstream industries and final consumers for this niche use was not different from the industry overall. If this were not the case, then the downstream industries that would be affected from the supply restriction would be different from what was modeled. The model also assumed that industries and final consumers want to return to their original consumption patterns, which might not always be the case, especially in the long term. There were also inherent assumptions regarding which industries gallium and germanium consumption were linked to in the model. Additionally, this analysis was specific to the disruption of gallium and germanium metals, compounds, and wafers and not the devices and products that contain these mineral commodities. Therefore, the results do not account for any disruptions in the availability of such downstream devices and finished products that were produced outside of the United States that may no longer be available for trade due to China restricting exports of the raw materials.

Despite these limitations, the results presented here provide an assessment that could be useful in making decisions regarding various mitigation strategies. For example, with the results from this analysis, a cost-benefit analysis can be performed to determine levels of maintaining or expanding strategic inventories. Similarly, plans for new plants to recover gallium and germanium can be assessed on a quantitative basis. This is noteworthy given that most of the gallium and germanium present in mined ores are not currently recovered (Licht and others, 2015; Frenzel and others, 2016, 2017). Similarly, while significant amounts of gallium and germanium are recycled as new scrap during fabrication and manufacturing, there is very limited postconsumer or end-of-life recycling of either element (Graedel and others, 2011; Licht and others, 2015; Mir and others, 2022). There is thus great potential for increasing and diversifying supplies, with several new sources of gallium and germanium being proposed or developed. For example, in late 2023, a newly built hydrometallurgical facility in southeastern Democratic Republic of the Congo noted that it had the capability of providing 30 percent of global germanium supply from processed slag (Société congolaise pour le traitement du terril de Lubumbashi, [undated]), although it was unclear if any production had taken place. Domestically, a zinc smelter in Clarksville, Tennessee, which already produces a germanium concentrate for export, was assessing the feasibility of a $150 million project to recover what it believes would be as much as 80 percent of annual U.S. consumption of gallium and germanium (Nyrstar, 2024). This model can be used to analyze various policies or incentives against the risks or costs of inaction for specific projects. Furthermore, when extended to include other mineral commodities, this analysis could be used to determine the U.S. list of critical minerals (Nassar and Fortier, 2021), which is a U.S. government-wide prioritized list of commodities of most concern that has provided the basis for various actions and policies, such as the Infrastructure Investment and Jobs Act of 2021 (Public Law 117–58; 135 Stat. 429) and the Inflation Reduction Act of 2022 (Public Law 117–169; 136 Stat. 1818).

References Cited

Bauer, D., Khazdozian, H., Mehta, J., Nguyen, R.T., Severson, M.H., Vaagensmith, B.C., Toba, L., Zhang, B., Hossain, T., Sibal, A.P., Smith, B.J., Riddle, M.E., Graziano, D.J., Mathew, T., Cuscaden, P., Dai, Q., Iloeje, C., Edgemon, L., Sarna, C., and Quaresima, J., 2023, Critical materials assessment: U.S. Department of Energy DE–AC07–05ID14517, 240 p., accessed July 30, 2024, at https://inldigitallibrary.inl.gov/sites/sti/sti/Sort_66849.pdf.

Board of Governors of the Federal Reserve System, 2023, Industrial production and capacity utilization—G.17: Board of Governors of the Federal Reserve System data, accessed August 11, 2023, at https://www.federalreserve.gov/releases/g17/caputl.htm.

Bureau of Economic Analysis, 2023, GDP by industry: U.S. Bureau of Economic Analysis interactive data tables, accessed July 30, 2024, at https://www.bea.gov/itable/gdp-by-industry.

Congressional Budget Office, 2024, Real potential gross domestic product [GDPPOT]: Congressional Budget Office data, accessed July 30, 2024, at https://fred.stlouisfed.org/series/GDPPOT.

Feldman, D., Zuboy, J., Dummit, K., Stright, D., Heine, M., Mirletz, H., and Margolis, R., 2024, Winter 2024 solar industry update: National Renewable Energy Laboratory, 60 p., accessed July 30, 2024, at https://www.nrel.gov/docs/fy24osti/88780.pdf.

Frenzel, M., Ketris, M.P., Seifert, T., and Gutzmer, J., 2016, On the current and future availability of gallium: Resources Policy, v. 47, p. 38–50, accessed July 30, 2024, at https://doi.org/10.1016/j.resourpol.2015.11.005.

Frenzel, M., Mikolajczak, C., Reuter, M.A., and Gutzmer, J., 2017, Quantifying the relative availability of high-tech by-product metals—The cases of gallium, germanium and indium: Resources Policy, v. 52, p. 327–335, accessed July 30, 2024, at https://doi.org/10.1016/j.resourpol.2017.04.008.

Ghosh, A., 1958, Input-output approach in an allocation system: Economica, v. 25, no. 97, p. 58–64, accessed July 30, 2024, at https://doi.org/10.2307/2550694.

Graedel, T.E., Allwood, J., Birat, J.-P., Buchert, M., Hageluken, C., Reck, B.K., Sibley, S.F., and Sonnemann, G., 2011, What do we know about metal recycling rates?: Journal of Industrial Ecology, v. 15, no. 3, p. 355–366, accessed July 30, 2024, at https://doi.org/10.1111/j.1530-9290.2011.00342.x.

Graedel, T.E., Harper, E.M., Nassar, N.T., Nuss, P., and Reck, B.K., 2015, Criticality of metals and metalloids: Proceedings of the National Academy of Sciences of the United States of America, v. 112, no. 14, p. 4257–4262, accessed July 30, 2024, at https://doi.org/10.1073/pnas.1500415112.

Grohol, M., and Veeh, C., 2023, Study on the critical raw materials for the EU—2023—Final report: European Commission Directorate-General for Internal Market, Industry, Entrepreneurship and SMEs, 152 p., accessed July 30, 2024, at https://doi.org/10.2873/725585.

Guberman, D.E., 2010–16, Germanium, in Metals and minerals: U.S. Geological Survey Minerals Yearbook 2007–14, v. I, chap. 30, [variously paginated], accessed July 30, 2024, at https://www.usgs.gov/centers/national-minerals-information-center/germanium-statistics-and-information.

Guberman, D.E., and Thomas, C.L., 2017, Germanium, in Metals and minerals: U.S. Geological Survey Minerals Yearbook 2015, v. I, chap. 30, p. 30.1–30.7, accessed July 30, 2024, at https://www.usgs.gov/centers/national-minerals-information-center/germanium-statistics-and-information.

Gulley, A.L., Nassar, N.T., and Xun, S., 2018, China, the United States, and competition for resources that enable emerging technologies: Proceedings of the National Academy of Sciences of the United States of America, v. 115, no. 16, p. 4111–4115, accessed July 30, 2024, at https://doi.org/10.1073/PNAS.1717152115.

Horowitz, K.J., and Planting, M.A., 2006, Concepts and methods of the input-output accounts [updated April 2009]: Bureau of Economic Analysis, 266 p., accessed July 30, 2024, at https://www.bea.gov/sites/default/files/methodologies/IOmanual_092906.pdf.

Jaskula, B.W., 2010–23, Gallium, in Metals and minerals: U.S. Geological Survey Minerals Yearbook 2007–21, v. I, chap. 27, [variously paginated], accessed July 30, 2024, at https://www.usgs.gov/centers/national-minerals-information-center/gallium-statistics-and-information.

Jowitt, S.M., 2020, Covid-19 and the global mining industry: SEG Discovery, v. 122, p. 33–41, accessed July 30, 2024, at https://doi.org/10.5382/SEGnews.2020-122.fea-02.

Kalantzakos, S., 2020, The race for critical minerals in an era of geopolitical realignments: The International Spectator, v. 55, no. 3, p. 1–16, accessed July 30, 2024, at https://doi.org/10.1080/03932729.2020.1786926.

Khurshid, A., Chen, Y., Rauf, A., and Khan, K., 2023, Critical metals in uncertainty—How Russia-Ukraine conflict drives their prices?: Resources Policy, v. 85, part B, August, article 104000, 10 p., accessed July 30, 2024, at https://doi.org/10.1016/j.resourpol.2023.104000.

Ku, A.Y., Loudis, J., and Duclos, S.J., 2018, The impact of technological innovation on critical materials risk dynamics: Sustainable Material Technology, v. 15, p. 19–26, accessed July 30, 2024, at https://doi.org/10.1016/j.susmat.2017.11.002.

Li, M., Lenzen, M., Pedauga, L.E., and Malik, A., 2022, A minimum-disruption approach to input-output disaster analysis: Spatial Economic Analysis, v. 17, no. 4, p. 446–470, accessed July 30, 2024, at https://doi.org/10.1080/17421772.2022.2056231.

Licht, C., Peiró, L.T., and Villalba, G., 2015, Global substance flow analysis of gallium, germanium, and indium—Quantification of extraction, uses, and dissipative losses within their anthropogenic cycles: Journal of Industrial Ecology, v. 19, no. 5, p. 890–903, accessed July 30, 2024, at https://doi.org/10.1111/jiec.12287.

Løvik, A.N., Restrepo, E., and Müller, D.B., 2015, The global anthropogenic gallium system—Determinants of demand, supply and efficiency improvements: Environmental Science and Technology, v. 49, no. 9, p. 5704–5712, accessed July 30, 2024, at https://doi.org/10.1021/acs.est.5b00320.

Manley, R.L., Alonso, E., and Nassar, N.T., 2022a, A model to assess industry vulnerability to disruptions in mineral commodity supplies: Resources Policy, v. 78, September, article 102889, p., accessed July 30, 2024, at https://doi.org/10.1016/j.resourpol.2022.102889.

Manley, R.L., Alonso, E., and Nassar, N.T., 2022b, Examining industry vulnerability—A focus on mineral commodities used in the automotive and electronics industries: Resources Policy, v. 78, September, article 102894, 8 p., accessed July 30, 2024, at https://doi.org/10.1016/j.resourpol.2022.102894.

Ministry of Commerce and General Administration of Customs [China], 2023, Implementation of export controls on gallium and germanium related items [in Chinese]: Ministry of Commerce and General Administration of Customs announcement 23, accessed October 2, 2023, at http://www.mofcom.gov.cn/article/zwgk/gkzcfb/202307/20230703419666.shtml.

Mir, S., Vaishampayan, A., and Dhawan, N., 2022, A review on recycling of end-of-life light-emitting diodes for metal recovery: Journal of the Minerals Metals & Materials Society [JOM], v. 74, p. 599–611, accessed July 30, 2024, at https://doi.org/10.1007/s11837-021-05043-9.

Nassar, N.T., 2023, Minerals for a changing world: Elements, v. 19, p. 342–344, accessed August 15, 2024, at https://doi.org/10.2138/gselements.19.6.342.

Nassar, N.T., and Fortier, S.M., 2021, Methodology and technical input for the 2021 review and revision of the U.S. critical minerals list: U.S. Geological Survey Open-File Report 2021–1045, 31 p., accessed July 30, 2024, at https://doi.org/10.3133/ofr20211045.

Nassar, N.T., Alonso, E., and Brainard, J., 2020a, Investigation of U.S. foreign reliance on critical minerals—U.S. Geological Survey technical input document in response to Executive Order No. 13953 signed September 30: U.S. Geological Survey Open-File Report 2020–1127, 37 p., accessed July 30, 2024, at https://doi.org/10.3133/ofr20201127.

Nassar, N.T., Brainard, J., Gulley, A., Manley, R., Matos, G., Lederer, G., Bird, L.R., Pineault, D., Alonso, E., Gambogi, J., and Fortier, S.M., 2020b, Evaluating the mineral commodity supply risk of the U.S. manufacturing sector: Science Advances, v. 6, no. 8, article eaay8647, 11 p., accessed July 30, 2024, at https://doi.org/10.1126/sciadv.aay8647.

Nassar, N.T., Graedel, T.E., and Harper, E.M., 2015, By-product metals are technologically essential but have problematic supply: Science Advances, v. 1, no. 3, article e1400180, 10 p., accessed July 30, 2024, at https://doi.org/10.1126/sciadv.1400180.

National Research Council, 2008, Minerals, critical minerals, and the U.S. economy: The National Academy of Sciences report, prepared by the National Research Council, 246 p., accessed July 30, 2024, at https://nap.nationalacademies.org/catalog/12034/minerals-critical-minerals-and-the-us-economy.

Nyrstar, 2024, Nyrstar Clarksville: Nyrstar web page, accessed July 30, 2024, at https://www.nyrstar.com/operations/metals-processing/nyrstar-clarksville.

Oosterhaven, J., 1988, On the plausibility of the supply-driven input-output model: Journal of Regional Science, v. 28, no. 2, p. 203–217, accessed July 30, 2024, at https://doi.org/10.1111/j.1467-9787.1988.tb01208.x.

Oosterhaven, J., 2017, On the limited usability of the inoperability IO model: Economic Systems Research, v. 29, no. 3, p. 452–461, accessed July 30, 2024, at https://doi.org/10.1080/09535314.2017.1301395.

Oosterhaven, J., and Bouwmeester, M.C., 2016, A new approach to modeling the impact of disruptive events: Journal of Regional Science, v. 56, no. 4, p. 583–595, accessed July 30, 2024, at https://doi.org/10.1111/jors.12262.

Prajapati, P., and Balamurugan, S., 2023, Leveraging GaN for DC–DC power modules for efficient EVs—A review: IEEE Access : Practical Innovations, Open Solutions, v. 11, p. 95874–95888, accessed July 30, 2024, at https://doi.org/10.1109/ACCESS.2023.3311266.

Project Blue Group Ltd., 2023, Gallium market service: Project Blue Group Ltd. web page, accessed July 30, 2024, at https://projectblue.com/subscriptions/critical-materials/gallium.

Schrijvers, D., Hool, A., Blengini, G.A., Chen, W.-Q., Dewulf, J., Eggert, R., van Ellen, L., Gauss, R., Goddin, J., Habib, K., Hagelüken, C., Hirohata, A., Hofmann-Amtenbrink, M., Kosmol, J., Le Gleuher, M., Grohol, M., Ku, A., Lee, M.-H., Liu, G., Nansai, K., Nuss, P., Peck, D., Reller, A., Sonnemann, G., Tercero., L., Thorenz, A., and Wäger, P.A., 2020, A review of methods and data to determine raw material criticality: Resources, Conservation & Recycling, v. 155, April, article 104617, 17 p., accessed July 30, 2024, at https://doi.org/10.1016/j.resconrec.2019.104617.

Shojaeddini, E., Alonso, E., and Nassar, N.T., 2024, Estimating price elasticity of demand for mineral commodities used in lithium-ion batteries in the face of surging demand: Resources Conservation Recycling, v. 207, August, article 107664, 9 p., accessed July 30, 2024, at https://doi.org/10.1016/j.resconrec.2024.107664.

Société congolaise pour le traitement du terril de Lubumbashi, [undated], STL—Home: Société congolaise pour le traitement du terril de Lubumbashi web page, accessed July 30, 2024, at https://www.stlgcm.com/.

Thomas, C.L., 2018–23, Germanium, in Metals and minerals: U.S. Geological Survey Minerals Yearbook 2016–19, v. I, chap. 30, [variously paginated], accessed July 30, 2024, at https://www.usgs.gov/centers/national-minerals-information-center/germanium-statistics-and-information.

U.S. Census Bureau, 2022, 2018–2021 annual survey of manufactures (ASM)—Tables: U.S. Census Bureau data, accessed October 11, 2023, at https://www.census.gov/data/tables/time-series/econ/asm/2018-2021-asm.html.

U.S. Census Bureau, 2023, 2017 NAICS sector 31-33—Manufacturing: U.S. Census Bureau data, accessed December 5, 2023, at https://www.census.gov/data/tables/2017/econ/economic-census/naics-sector-31-33.html.

U.S. Geological Survey, 2008–24, Mineral commodity summaries 2008–24: U.S. Geological Survey, accessed July 30, 2024, at https://www.usgs.gov/centers/national-minerals-information-center/mineral-commodity-summaries.

U.S. Geological Survey, [undated], Commodity statistics and information: U.S. Geological Survey National Minerals Information Center web page, accessed August 26, 2024, at https://www.usgs.gov/centers/national-minerals-information-center/commodity-statistics-and-information.

Yole Développement, 2018, GaAs wafer and epiwafer market—RF, photonics, LED, and PV applications 2020: Yole Développement market and technology report, accessed July 30, 2024, at https://www.everythingrf.com/research-reports/details/47-gaas-wafer-and-epiwafer-market-rf-photonics-led-display-and-pv-applications-2020.

Yole Développement, 2020, GaN RF market—Applications, players, technology and substrates—Forecast period 2019–2025: Yole Développement market and technology report, accessed July 30, 2024, at https://www.everythingrf.com/research-reports/details/40-gan-rf-market-applications-players-technology-and-substrates-2020.

Appendix 1. Supplemental Information for Quantifying Potential Effects of China’s Gallium and Germanium Export Restrictions on the U.S. Economy

Estimating Postdisruption Equilibrium Quantities and Prices

To determine equilibrium quantities and prices after a disruption, by using price elasticities of supply and demand, two basic log-linear supply (eq. 1.1) and demand (eq. 1.2) equations were used, as follows:

where S and D refer to the supply and demand respectively, Q refers to quantity, P refers to price, ε refers to price elasticity, and α and β are terms that account for all other variables that affect supply and demand, respectively.At initial equilibrium, before the disruption, the following was obtained:

A constant supply shift of magnitude (ΔQS) or relative magnitude (nS) can be defined as follows, where the shifted supply curve is :

Similarly, a constant demand shift of magnitude (ΔQD) or relative magnitude (nD) can be defined as follows, where the shifted demand curve is :

These supply and demand shifts were provided exogenously based on the scenario being examined and were assessed after accounting for available inventories that abated some or all the disruptions (for example, the inventory-adjusted shift in supply was the initial shift less any inventory releases). With these shifts in the supply and demand curves, the new equilibrium price (P′) was determined, as follows:

This nonlinear relation among price elasticities, price ratios, and relative shifts in the supply and demand curves was solved empirically to determine the new equilibrium price.With the new equilibrium price, the change in quantity from the initial equilibrium to the new equilibrium on an absolute (ΔQ′) and a relative (n′) basis was determined by using the demand curve, as follows:

The relative change in quantity from the initial to the new equilibrium quantity can also be determined in terms of the supply curve using the same approach:An assumption in the above derivation was that the price elasticity of supply is constant and that there was sufficient excess production capacity. However, that assumption was modified by noting that there was finite excess production capacity (κ), after which supply could not be increased regardless of the commodity’s price. On the predisruption supply curve, this would occur at a certain price (P*) at which all excess capacity would have been used, as follows:

The quantity (Q*) that this price would yield on the shifted demand curve was determined, as follows: The relative change in quantity necessary to get to this point () was defined as follows: Therefore, if , then the new equilibrium quantity became the initial equilibrium quantity plus all the excess capacity less the amount that was disrupted: This new quantity was set equal to the shifted demand curve to find the new equilibrium price: Using the new equilibrium price, the relative quantity shift to the new equilibrium (n′) was calculated by using equation 1.21: Note that the difference between n′ and nS represents the relative quantity of the excess production capacity that was utilized postdisruption (κu), which can be obtained from equation 1.22 or 1.34. Also note that, if there was no shift in the demand curve and if , then the new equilibrium price simplifies to:Empirical estimation of price elasticities.—Two general approaches to estimate the price elasticity of demand and price elasticity of supply for gallium and germanium were used. First, for the price elasticity of demand estimate with panel data, the demand elasticities were estimated by using a static framework, because the data used in the analysis lack a sufficiently long-time dimension to employ dynamic models. To tackle potential simultaneity issues of the price and consumption/production variables, a two-stage least-square and instrumental variable approach was employed. Following Shojaeddini and others (2024), the two-stage least-square regression was as follows:

In the first stage, the mineral commodity price (p) at time t and within sector i was determined through a function incorporating instrumental variable (Z) and other control variables (X). Subsequently, in the second stage, the estimation of the quantity demanded (d) for the mineral commodity involved utilizing the forecasted price () from the first stage alongside additional control variables. To facilitate the analysis, the variables were transformed logarithmically, allowing the estimated price coefficient (ε) to offer insights into the price elasticity of demand. Constants α0 and β0 denoted general terms, and αi and βi represented sector-specific constant terms referred to as sector-level fixed effects. Parameters αj and ακ denoted the impacts of control variables and instrumental variables on commodity price, respectively, while βj represented the influence of control variables on commodity demand. Furthermore, the terms vt and et served as error components in the model.

For the estimation of the price elasticities with time series data, an autoregressive distributed lag model was employed. This model estimates the production or consumption variable on its own lagged values, as well as on the current and lagged values of other control variables. Following Pesaran and Shin (1999) and Pesaran and others (2001), an autoregressive distributed lag (ρ, h1, h2, …, hn) model has the following general form:

where qt represented the commodity’s production or consumption quantity for year t; X was a vector of other explanatory variables, including the commodity’s price; ρ represented the lag order for the dependent variable; h was the lag order for other variables that was not necessarily the same for each explanatory variable (n); and ω and β′ were the corresponding coefficients for q and X, respectively.The error correction version of the autoregressive distributed lag model was represented by the following:

where Δ was the first difference, ECT = [qt−1 – λ′Xt−1] was the error correction term, and θ was the speed of adjustment coefficient. The first part of the equation with θ and λ represented the long-run relationship, and the second part with ω and β represented the short-run dynamics of the model. Due to potential simultaneity issues, the autoregressive distributed lag model was estimated in two stages using an instrumental variable approach as previously described.A structural break test (Ditzen and others, 2021) was used to examine whether there have been changes in the model parameters from significant disruptive events and to determine when these changes occurred. An interaction term was introduced between the price variable and a binary variable to indicate the occurrence of the structural change. By integrating this interaction term, which links the mineral commodity price variable with a binary variable reflecting the identified structural break in the market, the price elasticity of demand and price elasticity of supply variance before and after the structural break were evaluated. If the interaction term proved statistically insignificant in certain instances, the binary variable was incorporated into the regression to ensure parameter stability.

The price elasticity of demand of gallium was estimated by using global consumption data by each application sector obtained from Project Blue Group Ltd. (2023), and of germanium, from U.S. apparent consumption data from the U.S. Geological Survey (USGS; Kelly and Matos, 2023; Thomas, 2023; U.S. Geological Survey, 2024). The price elasticity of supply was estimated using the worldwide time series of primary production for each commodity (Jaskula, 2021; Kelly and Matos, 2023; Thomas, 2023; U.S. Geological Survey, 2024).

Gallium prices were derived from the average unit value of U.S. imports for low-purity gallium (U.S. Geological Survey, 2024). Germanium prices were from U.S. Geological Survey (2013, 2024) and reflected the average price of germanium metal (more than or equal to 99.99 percent) and unit value of U.S. imports.

For explanatory variables, the industrial production index for U.S. manufacturing was obtained from Board of Governors of the Federal Reserve System (2024). Silicon metal prices, bauxite, zinc, and coal production were from U.S. Geological Survey (2013, 2024). The results are summarized in tables 1.1 through 1.4. Each set of columns represents results derived from either a different estimation method or a different set of variables.

Table 1.1.

Estimation of price elasticity of demand of gallium.[The regression includes sector identification variables, which are binary variables representing each demand sector. Significance levels are denoted as *** (p-value<0.01), ** (p-value <0.05), and * (p-value <0.1). All monetary variables are adjusted for inflation using the world gross domestic product (GDP) deflator. GDP deflator is calculated using data from the World Bank Group, specifically world GDP constant in 2015 U.S. dollars purchasing power equivalent (World Bank Group, 2023a) and world GDP in current U.S. dollars (World Bank Group, 2023b). This deflator represents the global inflation rate, providing a measure of how much prices have increased on average across the world economy. SE, bootstrapped/heteroskedasticity and autocorrelation robust standard error; Ga, gallium; Si, silicon; LED, light-emitting diode; 2SLS, two-stage least squares estimation]

| Variable | Log(Ga consumption) | |

|---|---|---|

| Coefficient | SE | |

| Log(Ga real price) | −0.53* | 0.31 |

| LED penetration rate | 0.02*** | 0.00 |

| Log(Si metal real price) | 0.47* | 0.26 |

| Constant | 4.82*** | 0.67 |

| Number of observations | 50 | |

| Estimation method | 2SLS | |

| Ga price data basis (source) | Low-purity, primary gallium ore (U.S. Geological Survey, 2024) | |

| Instrumental variable | Bauxite production | |

| Adjusted coefficient of determination (R2) | 0.942 | |

| Weak identification test p-value | 0.001 | |

Table 1.2.

Estimation of price elasticity of supply of gallium.[The regression includes sector identification variables, which are binary variables representing each demand sector. Significance levels are denoted as *** (p-value<0.01), ** (p-value <0.05), and * (p-value <0.1). All monetary variables are adjusted for inflation using the world gross domestic product (GDP) deflator. GDP deflator is calculated using data from the World Bank Group, specifically world GDP constant in 2015 U.S. dollars purchasing power equivalent (World Bank Group, 2023a) and world GDP in current U.S. dollars (World Bank Group, 2023b). This deflator represents the global inflation rate, providing a measure of how much prices have increased on average across the world economy. Gallium price represents low purity gallium for recent years which has been extrapolated back using gallium average price (99.9999-percent-pure metal) from 1959 to 2000. Variables beginning with “Dum” (short for dummy) signify binary variables. They take the value of 1 after the year indicated following “Dum” in the variable’s name and remain at 0 otherwise. SE, bootstrapped/heteroskedasticity and autocorrelation robust standard error; Ga, gallium; Si, silicon; 2SLS, two-stage least squares estimation; ARDL, autoregressive distributed lag model; —, not applicable; t−1, previous year]

Table 1.3.

Germanium price elasticity of demand estimation.[The regression includes sector identification variables, which are binary variables representing each demand sector. Significance levels are denoted as *** (p-value<0.01), ** (p-value <0.05), and * (p-value <0.1). All monetary variables are adjusted for inflation using the world gross domestic product (GDP) deflator. GDP deflator is calculated using data from the World Bank Group, specifically world GDP constant in 2015 U.S. dollars purchasing power equivalent (World Bank Group, 2023a) and world GDP in current U.S. dollars (World Bank Group, 2023b). This deflator represents the global inflation rate, providing a measure of how much prices have increased on average across the world economy. SE, bootstrapped/heteroskedasticity and autocorrelation robust standard error; Ge, germanium; Si, silicon; 2SLS, two-stage least squares estimation; ARDL, autoregressive distributed lag model; t−1, previous year]

Table 1.4.

Germanium price elasticity of supply estimation.[The regression includes sector identification variables, which are binary variables representing each demand sector. Significance levels are denoted as *** (p-value<0.01), ** (p-value <0.05), and * (p-value <0.1). All monetary variables are adjusted for inflation using the world gross domestic product (GDP) deflator. GDP deflator is calculated using data from the World Bank Group, specifically world GDP constant in 2015 U.S. dollars purchasing power equivalent (World Bank Group, 2023a) and world GDP in current U.S. dollars (World Bank Group, 2023b). This deflator represents the global inflation rate, providing a measure of how much prices have increased on average across the world economy. Variables beginning with “Dum” (short for dummy) signify binary variables. They take the value of 1 after the year indicated following “Dum” in the variable’s name and remain at 0 otherwise. The interaction between the price variable and the binary variable shows changes in the price elasticity of demand following the specified year indicated by the structural break year. SE, bootstrapped/heteroskedasticity and autocorrelation robust standard error; Ge, germanium; Si, silicon; 2SLS, two-stage least squares estimation; ARDL, autoregressive distributed lag model; —, not applicable; t−1, previous year]

Gallium

World Production and Production Capacity

In addition to primary (low purity; figs. 1.1, 1.2, and 1.3) gallium production and production capacities, refined (high purity) and secondary (new scrap recycled) gallium production and production capacities were reported or estimated based on various sources (table 1.5).

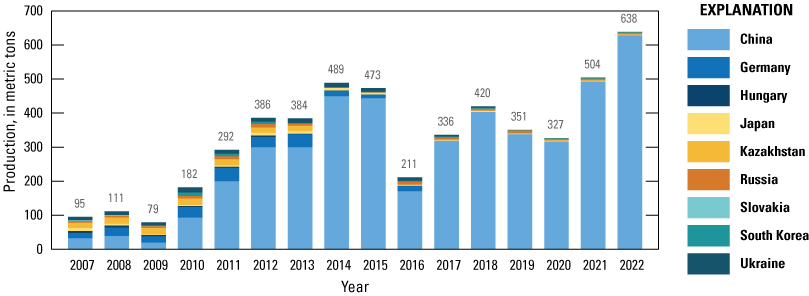

Graph showing world production of primary (low-purity) gallium, by country, from 2007 to 2022. Data are from Jaskula (2021) and U.S. Geological Survey (2024), with updated numbers for China from Asian Metals Ltd. (2023a).

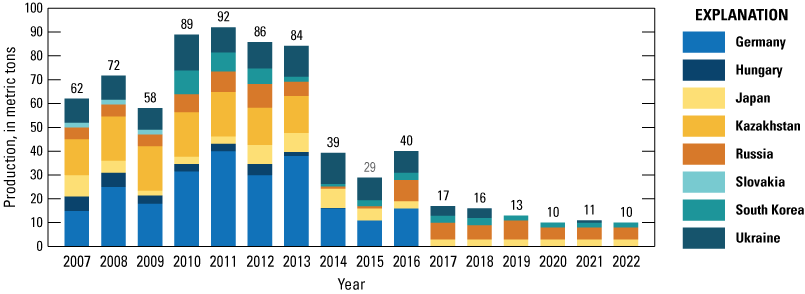

Graph showing production of primary (low-purity) gallium outside of China from 2007 to 2022. Data are from Jaskula (2021) and U.S. Geological Survey (2024).

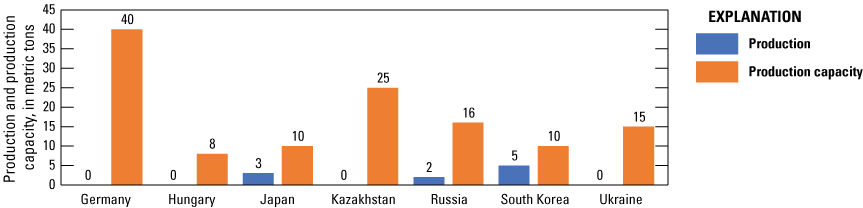

Graph showing production and production capacity of primary (low-purity) gallium outside of China, in 2022. Data are from Jaskula (2021) and U.S. Geological Survey (2024).

Table 1.5.

Primary (low purity), primary (high purity) refined, and secondary refined production and production capacities by country, circa 2021/2022[Data are from Rongguo and others (2016), Roskill Information Services Ltd. (2020), Jaskula (2021), Asian Metals Ltd. (2023a), Neo Performance Materials (2023), Project Blue Group Ltd. (2023), Japan Organization for Metals and Energy Security (2024), U.S. Geological Survey (2024), or estimated by the authors using trade data (Zen Innovations AG (2024)). t, metric ton]

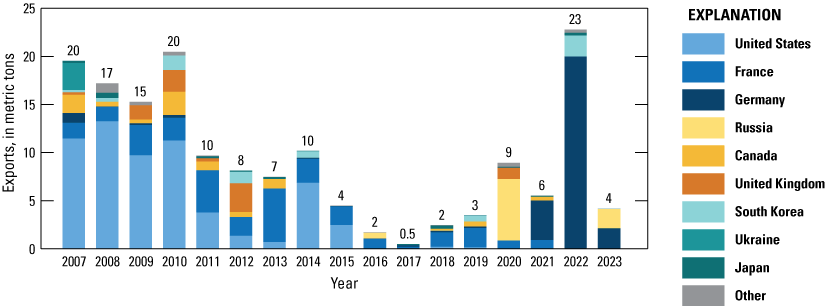

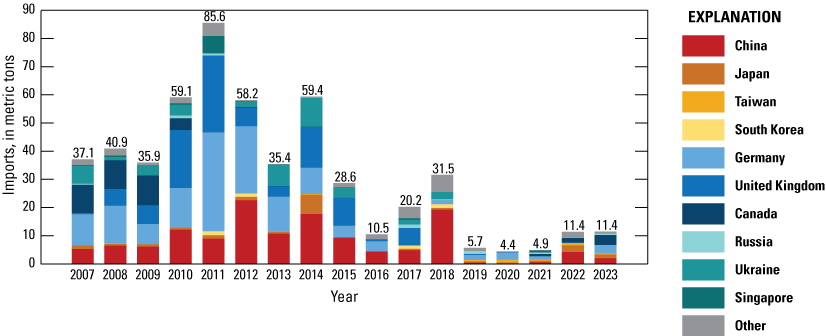

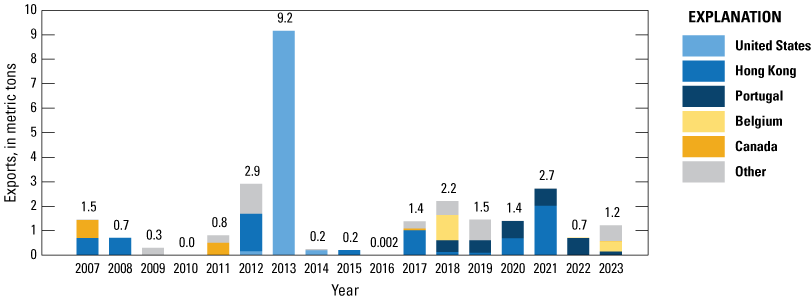

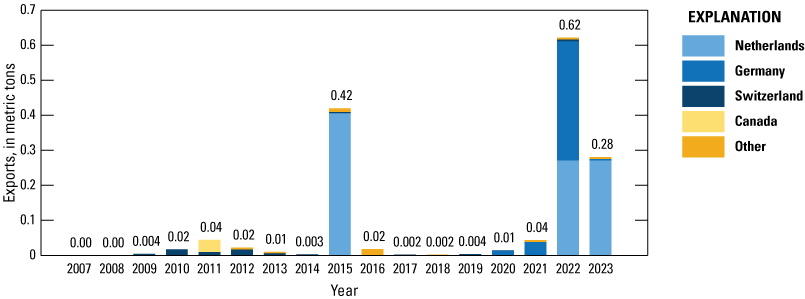

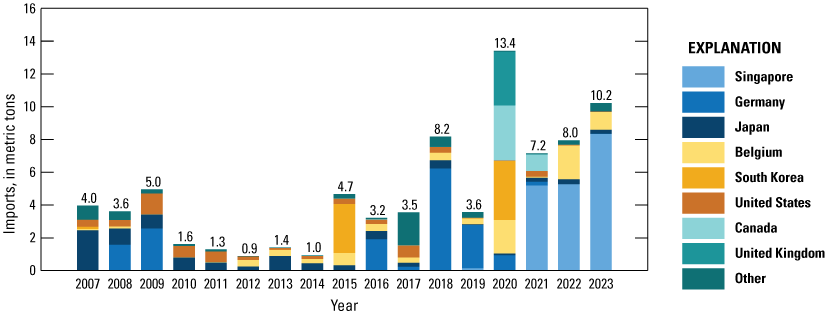

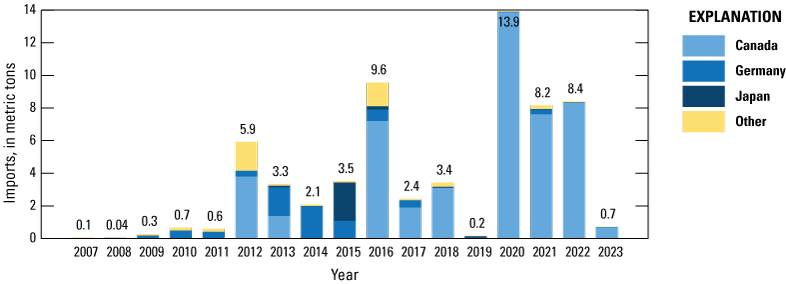

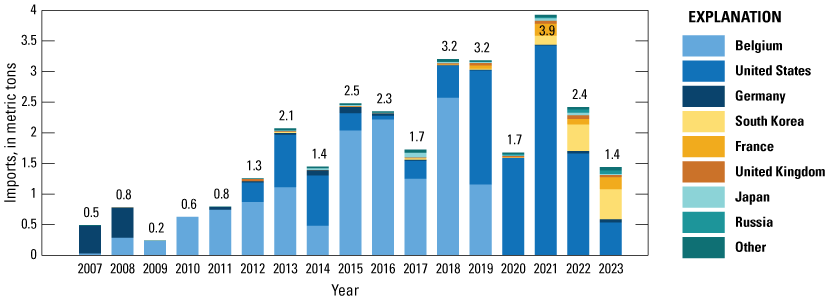

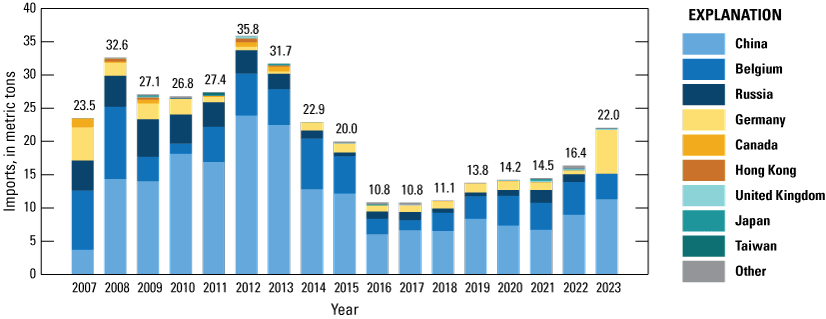

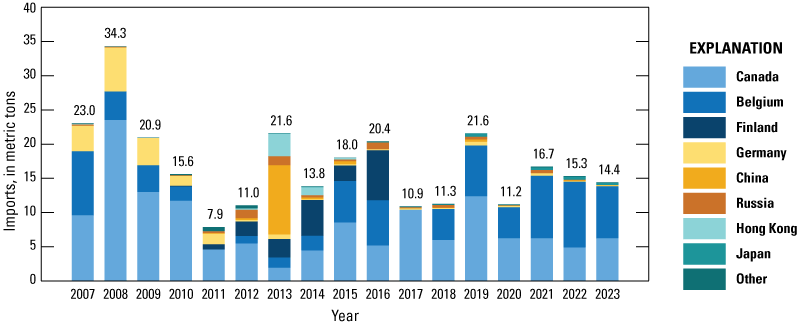

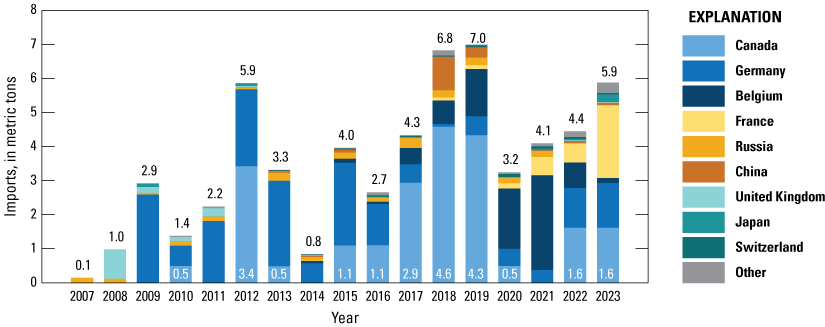

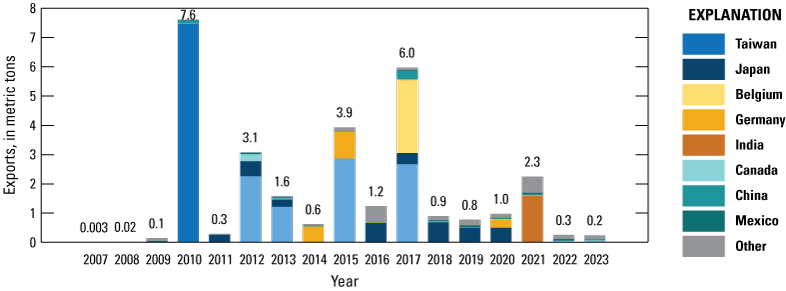

China’s Trade of Gallium Products