Methodology and Technical Input for the 2025 U.S. List of Critical Minerals—Assessing the Potential Effects of Mineral Commodity Supply Chain Disruptions on the U.S. Economy

Links

- Document: Report (3.17 MB pdf) , HTML , XML

- Data Release: USGS data release - U.S. Geological Survey Minerals Yearbook data for select mineral commodities referenced in “U.S. Geological Survey Methodology and Technical Input for the 2025 U.S. List of Critical Minerals—Assessing the Potential Effects of Mineral Commodity Supply Chain Disruptions on the U.S. Economy”

- Version History: Version History (3.01 KB txt)

- NGMDB Index Page: National Geologic Map Database Index Page (html)

- Download citation as: RIS | Dublin Core

Acknowledgments

The authors would like to thank Lee Bray, Chad Friedline, Robert Goodin, Ashley Hatfield, Daniel Hayba, Stephen Jasinski, Brian Jaskula, Natalie Juda, Kateryna Klochko, Graham Lederer, Timothy O’Brien, Emily Schnebele, Ruth Schulte, Robert R. Seal II, Miriam Stevens, and Colin Williams at the U.S. Geological Survey for their input and feedback. The authors would also like to thank the U.S. Bureau of Economic Analysis for providing detailed input-output tables for 2023, which were not publicly available at the time of publication, for use in this study.

Abstract

The Secretary of the Interior, acting through the Director of the U.S. Geological Survey, is tasked by section 7002 (“Mineral Security”) of title VII (“Critical Minerals”) of the Energy Act of 2020 (Public Law 116–260, December 27, 2020, 116th Congress) with reviewing and revising the methodology used to evaluate mineral commodity supply risk and the U.S. List of Critical Minerals (LCM) no less than every 3 years. Following two previous LCM assessments, this analysis represents the latest technical input for evaluating each mineral commodity’s supply risk and determining their recommended status on the LCM. We evaluated mineral commodity supply risk using two criteria: (1) an economic effects assessment that quantified the potential effects of various trade disruption scenarios on the U.S. economy, and (2) an examination of whether the mineral commodity’s U.S. supply chain relied on a sole domestic producer that represented a single point of failure. For the first criterion, postdisruption equilibrium quantities and prices for each mineral commodity were calculated based on their price elasticities of supply and demand and the availability of excess production capacity for each yearlong foreign trade disruption scenario. Subsequently, a nonlinear optimization routine was used with detailed economic input-output tables to estimate the potential economic effects on the U.S. economy of over 1,200 scenarios for 84 mineral commodities. After accounting for the probability of each scenario’s occurrence, the overall results are presented in terms of changes in U.S. gross domestic product (GDP) by individual industry and the economy overall. The results, which ranged from a net decrease in U.S. GDP of nearly $4.5 billion to a net increase of $33 million, largely reflect U.S. import dependency and world production concentration. Using the Jenks natural breaks optimization method, a statistical classification technique, we categorized the mineral commodities into several classes based on this overall risk quantification. Mineral commodities with annualized probability-weighted net decreases in U.S. GDP greater than $2 million were recommended for inclusion on the LCM. If a mineral commodity did not meet the threshold for inclusion on the LCM under the first criterion, its domestic supply chain was examined under the second criterion, which recommended a mineral commodity for inclusion on the LCM if there was only a single domestic producer. Ultimately, the two criteria resulted in the recommendation of the addition of six mineral commodities (in descending risk order, potash, silicon, copper, silver, rhenium, and lead) to and the removal of two mineral commodities (arsenic and tellurium) from the LCM. By using an economic effects assessment, the results of this analysis provide a prioritization that can also be compared directly against other risk analyses and the cost of various risk mitigation strategies.

Plain Language Summary

To quantify the risks associated with potential disruptions and to recommend mineral commodities for inclusion on the updated U.S. List of Critical Minerals, as required by the Energy Act of 2020, the U.S. Geological Survey developed an economic model to estimate the potential effects of foreign trade disruptions of mineral commodities on the U.S. economy. The results of the study recommend the addition of six mineral commodities (in descending risk order, potash, silicon, copper, silver, rhenium, and lead) to and the removal of two mineral commodities (arsenic and tellurium) from the List of Critical Minerals. The analysis also provides a prioritization based on the results. The economic model has several advantages over previous assessments including the ability to directly compare the results against other economic risks and the costs of initiatives aimed at reducing the risks.

Introduction

Reliable supplies of mineral commodities, which are used in a myriad of technologies—old and new—are necessary for maintaining and growing the U.S. economy. The concentration of mineral commodity production in a few countries and the high degree of reliance of the United States on imports from these countries increases the risks associated with foreign supply disruptions (Nassar and others, 2020). These risks have been exemplified in recent months as the Ministry of Commerce of the People’s Republic of China (MOFCOM) has placed controls and outright bans on the exports of several mineral commodities including antimony, gallium, and germanium to the United States (Ministry of Commerce of the People’s Republic of China, 2024).

The Secretary of the Interior, acting through the Director of the U.S. Geological Survey, is tasked by section 7002 (“Mineral Security”) of title VII (“Critical Minerals”) of the Energy Act of 2020 (Public Law 116–260, December 27, 2020, 116th Congress) with reviewing and revising the methodology used to evaluate mineral commodity supply risk and the U.S. List of Critical Minerals (LCM) no less than every 3 years. In fulfilling part of the requirements of the Energy Act of 2020, the U.S. Geological Survey (USGS) provides the technical input for identifying mineral commodities whose supply disruption poses the greatest risk to the U.S. economy and national security. The Energy Act of 2020 defines “critical minerals” as the minerals, elements, substances, or materials that “(i) are essential to the economic or national security of the United States; (ii) the supply chain of which is vulnerable to disruptions (including restrictions associated with foreign political risk, abrupt demand growth, military conflict, violent unrest, anti-competitive or protectionist behaviors, and other risks throughout the supply chain); and (iii) serve an essential function in the manufacturing of a product (including energy technology-, defense-, currency-, agriculture-, consumer electronics-, and healthcare-related applications), the absence of which would have significant consequences for the economic or national security of the United States” (Public Law 116–260, section 7002(c)(4)(A)). The Energy Act of 2020 followed Executive Order 13817, “A Federal Strategy To Ensure Secure and Reliable Supplies of Critical Minerals” (3 CFR, 2017 Comp, p. 397–399), which tasked the Secretary of the Interior with submitting to the Federal Register a draft list of minerals determined to be critical. The methodology used in the first List of Critical Minerals (LCM) in 2018 involved two quantitative criteria (the concentration of global mineral commodity production and U.S. net import reliance) and a qualitative examination of the importance of each mineral commodity’s use (Fortier and others, 2018). After the passage of the Energy Act of 2020, a new methodology that provided several enhancements to the original approach was used in determining the second LCM in 2022 (Nassar and Fortier, 2021). Using a risk modeling framework, the second assessment retained the U.S. net import reliance indicator and weighted the previous global production concentration indicator by measures of each producing country’s willingness and ability to continue to supply the United States. In addition, it converted the qualitative examination of each mineral commodity’s importance into a quantitative assessment using data on each mineral commodity consuming industry’s contributions to U.S. gross domestic product (GDP) and gross operating surplus. It also added a criterion for including any mineral commodity on the LCM if there was only a single domestic producer, which represented a potential single point of failure (SPOF) within the mineral commodity’s domestic supply chain.

The analysis presented in this report takes another major step forward in assessing the risk associated with foreign trade disruptions. While the analysis presented here retains the same conceptual framework as the previous assessments, it moves away from normalized indicators and toward an economic effects assessment. In this approach, the risks associated with foreign trade disruptions are assessed probabilistically, and the results are provided in terms of expected (or probability-weighted) net decreases in U.S. GDP at the level of individual industries and the economy overall. Our analysis, which was conducted using data for year 2023 (unless otherwise noted), assessed over 1,200 scenarios for 84 mineral commodities.

Methods

We used two criteria in recommending a mineral commodity for inclusion on the LCM. One criterion assessed the potential economic effects of foreign trade disruptions on the U.S. economy. The other criterion evaluated whether there was a single producer of that mineral commodity (for example, a sole mine or refinery) in the United States (referred to as a SPOF). The methodology used to estimate the potential economic effects was primarily based on Nassar and others (2024) and consists of three stages: scenario quantification, equilibrium displacement modeling, and economic impacts modeling. These three stages of the economic effects assessment are discussed in detail below. If a mineral commodity did not meet the first criterion, its domestic supply chain was reviewed using the information presented in the USGS Mineral Commodity Summaries (U.S. Geological Survey, 2025a) to determine if there was a SPOF within its domestic supply chain. Details regarding specific sources and methods are found in the appendixes, which were initially published as a preprint (Nassar and others, 2025) before being edited and formatted for release in this version of this publication.

Stages of the Economic Effects Assessment

Scenario Quantification

The first stage of the economic effects assessment defined a specific set of scenarios. These scenarios were ones in which U.S. net imports (imports minus exports) for the mineral commodity of concern from each trading partner country were completely restricted for an entire year. A scenario was thus developed for each mineral commodity–restricting country pair if that country was also a producer of the mineral commodity. Any positive U.S. net imports for that mineral commodity (when summed across all forms included in the analysis) from non-producing countries were allocated to producing countries proportionally to their share of world production. This step was added to account for the fact that positive net imports from non-producing countries must have, at some point, originated from producing countries.

For each mineral commodity, annualized country-level global production and trade data were collected by production stage (for example, mining) or mineral-commodity form (for example, ores and concentrates). Data availability allowed for the assessment of 84 mineral commodities. Of these 84, 31 represent different stages or forms of 11 mineral commodity supply chains: aluminum (alumina, aluminum, and bauxite), chromium (chemicals, chromite, ferroalloys, and metal), cobalt (chemicals and metal), copper (mined and refined), graphite (natural and synthetic), fluorspar (acidspar and metspar), manganese (alloys, dioxide, high-purity sulfate, metal, ore), nickel (mined and primary refined), silicon (ferroalloys and metal), titanium (ferroalloys, metal, mineral concentrates, pigment, and sponge), and zinc (mined and smelted). Magnesium compounds and magnesium metal were treated as separate mineral commodity supply chains given their distinct sources and uses. Mineral production data included primary production and, if applicable and available, secondary (specifically, end-of-life or post-consumer recycling) production by country. Production data were mainly obtained from the most recent USGS publications, although other sources were used where necessary (refer to appendix 1 for details). For a few mineral commodities, secondary production data were only available by region or for the entire world. In cases where it was not possible to allocate these secondary production data to individual countries, the reported regional production quantities were treated as if they were a single entity in the scenario.

Global trade data were obtained from the Global Trade Tracker database (Zen Innovations AG, 2025) using the Harmonized Tariff Schedule of the United States (HTS) and Schedule B codes identified in appendix 2 for the imports and exports of each mineral commodity, respectively. The trade data were obtained from the U.S. perspective (meaning as reported by the United States) unless the trade data from the trade partner country’s perspective were determined to be more representative for the mineral commodity (refer to appendix 2 for details). Production and trade data were converted into elemental content (for example, the antimony content of antimony trioxide) to allow for summation across different chemical forms and were calculated net of any reimports or reexports (meaning that trade flows were calculated exclusive of the flows of commodities that were previously recorded as exports or imports, respectively, in substantiality the same condition) (International Trade Administration, 2015). Trade codes were selected to reflect the chemical forms (typically alloys, compounds, concentrates, metals, ore, and scrap) that were produced by the associated production processes up to the supply chain process associated with the identified consuming industries (as explained in the “Economic Impacts Modeling” section of this report). Additional notes and assumptions are provided in appendixes 1 and 2 for production and trade data, respectively.

Equilibrium Displacement Modeling

In the second stage of the economic effects assessment, the production and trade data were allocated to two regions or markets—the restricting country and the rest of the world—that varied by scenario. The quantity that was disrupted (∆Q) in each scenario (s) for each mineral commodity (c) was set equal to the U.S. net imports from the restricting country (NI) for the year. A postdisruption equilibrium price (P′) and quantity (Q′) for the rest of the world were determined based on (1) the quantity disrupted, (2) excess production capacity of the mineral commodity in the rest of the world (κROW), (3) the mineral commodity’s price elasticities of supply (εS) and demand (εD), and (4) the predisruption quantity of the mineral commodity available (Q). Specifically, the postdisruption equilibrium price relative to the predisruption price (P) was determined as follows:

where n was the relative shift in quantity available (). The predisruption quantity of the mineral commodity available (Q) was defined as the sum of the predisruption quantity that was produced by the rest of the world (ψROW) and the net imports from the restricting country (NI):This approach defined the system boundaries of the mineral commodity market that would be available to the United States, which varied by scenario because the definition (and, in turn, the net imports and production) of the rest of the world varied depending on which country was the restricting country. A scenario in which the restricting country was the sole producer of the mineral commodity would yield a relative shift in quantity available (n) of 100 percent. (Note that no such scenario was encountered in this analysis.) Establishing the system boundaries in this manner implicitly assumes that the mineral commodity produced by the non-restricting countries would be available and thus could be diverted to the United States. It also assumes that the restricting country applies its export restrictions extraterritorially, meaning that its exports to countries other than the United States are prohibited from being reexported to the United States. This assumption would also apply to downstream materials (for example, rare earth permanent magnets) that were included in the trade data, thereby effectively prohibiting non-restricting countries from exporting materials that they processed if the precursor materials were originally sourced from the restricting country.

Postdisruption equilibrium prices were determined numerically by setting equation 1 equal to equation 2. With the postdisruption equilibrium price, the relative change in the postdisruption equilibrium quantity, also referred to as the net disruption level (n′), was determined as follows:

If the specified scenario resulted in a supply disruption greater than the available excess capacity in the rest of the world (κROW), then equation 3 simplified to:This simplification was possible because the supply curve was assumed to become vertical at the point in which all excess capacity was used—a reflection of the inability to increase supplies in the short-term beyond the estimated capacities. Under such scenarios, the demand curve intercepts the vertical portion of the supply curve thereby allowing the postdisruption equilibrium price to be calculated directly:

The growth in the production of the rest of the world () that was necessary to achieve the postdisruption equilibrium quantity was calculated as follows:

The derivations of these equations are provided by Nassar and others (2024).Following Shojaeddini and others (2025), each mineral commodity’s price elasticities of supply and demand were estimated using fixed effects models for panel data and two-stage dynamic ordinary least-squares along with autoregressive distributed lag models for time-series data (refer to appendix 3 for a summary of the elasticities used in the analysis). Where possible, short-run (1-year) price elasticities were used, and price elasticities of demand were estimated to include inventory releases as a demand category.

Data on production capacity by country were obtained from published sources (refer to appendix 1) or, if not available, were estimated for each producing country based on historical production. Specifically, for the latter, production capacity for each currently producing country was assumed to equal its maximum production that was reported during the preceding 5-year period (2019–2023) divided by 80 percent to simulate an assumed capacity utilization rate. Additionally, a linear ramp-up time of 6 months was assumed to be required to reach the reported or estimated production capacity by country.

Economic Impacts Modeling

Three intermediate results for each scenario were obtained from the equilibrium displacement modeling (stage 2 of the economic effects assessment): the postdisruption equilibrium price, quantity, and the growth in production for the rest of the world. In the third stage of the economic effects assessment—the economic impacts modeling—these results were used with detailed economic input-output (IO) tables for the United States in a nonlinear optimization routine to estimate the potential effects of the scenarios on the U.S. economy (specifically, net decreases in U.S. GDP by industry). The intuition behind the model is that, in the event of a supply disruption, economic actors (be they final consumers, industries, or governments) will attempt to reestablish their economic activity patterns as closely as possible to their predisruption levels (Oosterhaven and Bouwmeester, 2016). As described by Nassar and others (2024), the objective function of the optimization model therefore attempted to minimize the change between the predisruption and postdisruption interindustry intermediate demand, final demand, and value added across all industries, as follows:

wherez and z′

were the predisruption and postdisruption interindustry intermediate demand, respectively;

y and y′

were the predisruption and postdisruption final demand, respectively;

v and v′

were the predisruption and postdisruption value added, respectively; and

i, j

were subscripts that indicate individual industries.

The decision variables in the model were each industry’s postdisruption output (x′). Each industry’s final postdisruption final demand (y′) was determined using the Leontief equation (Leontief, 1951), which provided the overall supply and demand equilibrium for the U.S. economy:

where I was the identity matrix and A was the industry-by-industry direct requirements matrix. Additionally, values for individual postdisruption interindustry intermediate demand (z′) were calculated using the direct requirements matrix:Data for each of the predisruption parameters of equations 7, 8, and 9 (all reported in current [2023] U.S. dollars) were available for the United States from the U.S. Bureau of Economic Analysis (BEA) at the detailed 402-industry level for years 2007, 2012, and 2017 (U.S. Bureau of Economic Analysis, 2025). The BEA industry groupings generally correspond to the definitions of the North American Industry Classification System (NAICS), which was developed under the auspices of the Office of Management and Budget to coordinate and publish industry data by Federal statistical agencies (U.S. Census Bureau, 2024). At the detailed level, an industry consists of establishments that are primarily engaged in similar processes to produce a narrowly defined category of products or services (for example, the “Computer storage device manufacturing” industry with NAICS code 334112). Multiple industries make up a subsector (for example, the “Computer and electronic product manufacturing [334]” subsector), which itself falls within a specific sector (for example, the “Manufacturing [31–33]” sector) of the economy (Office of Management and Budget, 2022). The BEA publishes updates to the IO tables annually but only at aggregated levels (U.S. Bureau of Economic Analysis, 2025). These aggregated data are based on estimated detailed IO tables, which were provided to the authors (U.S. Bureau of Economic Analysis, written comm., October 31, 2024). The most recent data provided (for year 2023) were used in this analysis.

The optimization routine was subjected to several constraints, including a mineral commodity availability constraint:

This constraint specified that the total quantity of the mineral commodity used by industries in the United States—calculated as the product of each consuming industry’s output and its mineral consumption ratio (m), summed across all industries—must equal the total postdisruption quantity of the mineral commodity (M′) that was available under the specified disruption scenario. The quantity of the mineral commodity that was available after the supply disruption was based on the predisruption quantity consumed in the United States (M) and the net disruption level (n′) that was derived in equilibrium displacement modeling:

The implicit assumption here is that the quantity that would be available for consumption in the United States decreases in the same relative proportion as that of the rest of the world (outside of the restricting country).

For each mineral commodity, the predisruption quantity that was consumed in the United States was calculated as the sum of domestic primary and secondary production, net imports, and changes in inventories. Data for each of these were obtained from the same sources as those listed in appendixes 1 and 2, with additional data for inventories obtained from the latest USGS Mineral Commodity Summaries (U.S. Geological Survey, 2025a) where applicable. The calculated or “apparent” consumption quantity was split into specific applications that were linked to individual industries. For example, the use of barite to increase the density of drilling mud in the petroleum industry was connected to the “Drilling oil and gas wells [213111]” BEA industry. As much as possible, we aligned the trade codes used in the equilibrium displacement model to the forms of the mineral commodities that would be purchased by (or the supply chain processes that directly precede) the selected BEA consuming industries. In certain cases, connections were made further downstream if the direct consuming industries were determined to be too broad to reasonably capture the use of the mineral commodity in the application. For example, cobalt metal’s use in high-performance “superalloys” was connected downstream to the “Aircraft engine and engine parts manufacturing [336412]” and the “Turbine and turbine generator set units manufacturing [333611]” industries rather than the “Iron and steel mills and ferroalloy manufacturing [331110]” industry. Details regarding the application fractions and the BEA industry connections are provided in appendix 4.

The monetary value of the trade of the mineral commodity was added to the value of domestic production and inventory releases to provide an estimate for the value of the apparent consumption. The monetary value of domestic production and inventory releases was calculated as the product of the quantities produced and released and the price noted in appendix 3 for each mineral commodity. In turn, an apparent consumption unit value was calculated as the ratio of the monetary value to the quantity of the calculated apparent consumption.

Even at the detailed 402‑industry level, not all the output of each identified BEA industry uses the mineral commodity in question. For example, not all of the output of the “Drilling oil and gas wells [213111]” industry uses barite, and not all of the output of the “Semiconductor and related device manufacturing [334413]” industry uses gallium or germanium. To address this issue, Nassar and others (2024) used modified mineral consumption ratios that account for the portion of each BEA industry’s output that used the mineral commodity in question. In this analysis, we instead performed a streamlined IO table expansion. Specifically, each consuming BEA industry was split into two industries: one that consumes the mineral commodity and the other that does not. Because IO table expansion requires extensive additional data regarding the newly formed industries’ inputs from and outputs to all other industries and final demand (data which were not readily available), simplifications were required. One simplification was that the newly formed industries had the same relative production recipe (in terms of monetary inputs per unit of output) as the original industry from which they were disaggregated. This meant that the columns of the direct requirements table for the two new industries were unchanged from the original. The other simplification was that the newly formed industries’ outputs to the other industries and to final demand were all split using the same proportion, which was based on the share of the original industry’s output that was estimated to have used the mineral commodity in question. These proportions, by industry and mineral commodity, were estimated mainly using data on the revenues generated from the sales of specific product(s) as defined by the North American Product Classification System (NAPCS) and reported in the 2017 Economic Census (U.S. Census Bureau, 2020) and the 2018–2021 Annual Survey of Manufactures (U.S. Census Bureau, 2022). Other sources and methods were used where the NAPCS data did not provide sufficient disaggregation for the mineral commodity. Details are provided in appendix 4. Note that the newly formed industries were remerged after running the optimization routine in order to report the results across a consistent set of 402 industries. With expanded IO tables, the mineral consumption ratio was calculated as the ratio of the quantity of the mineral commodity consumed by that industry relative to that industry’s output in U.S. dollars.

Another constraint used in the model was an industry production capacity constraint, which required each industry’s output to maintain a positive value that does not exceed that of its capacity (xc):

Each industry’s output capacity was calculated by dividing its predisruption output by its capacity utilization rate, u. Data regarding annual capacity utilization rates for industries within the manufacturing, mining, and electric and gas utilities sectors of the United States were obtained from the Board of Governors of the Federal Reserve System (2024). As explained by Nassar and others (2024), these data were available at the 3‑digit or 4‑digit NAICS subsector level or equivalent, whereas the BEA IO tables were reported at the 4-, 5-, or 6‑digit NAICS level equivalent. The capacity utilization data at the 3- and 4‑digit levels were thus applied to the most appropriate level or sublevel, accordingly. For the remaining industries outside of the manufacturing, mining, and electric and gas utilities sectors, the capacity utilization rate was set to 80 percent, which was approximately the average utilization rate across all sectors with capacity utilization data in 2023 (Board of Governors of the Federal Reserve System, 2024).

Each consuming industry’s postdisruption value added (its postdisruption contribution to U.S. GDP) was calculated as follows:

Changes to an industry’s value added were thus due to changes in both its output and its expenditure on the mineral commodity, with the latter being determined by changes in the mineral commodity’s price and the quantity consumed postdisruption. Although the changes in the mineral commodity’s price were determined in the equilibrium displacement model, changes in the quantity of the mineral commodity consumed were determined endogenously within the economic impacts model as it was a function of the consuming industry’s postdisruption output.

Because the demand curve for each mineral commodity was estimated using a single price elasticity, it was necessary to introduce a price maximum for mineral commodities with highly inelastic demand under scenarios in which the quantity restricted was large enough that all excess production capacity in the rest of the world was used (in other words, where a nearly vertical demand curve intersected the vertical portion of the supply curve). The price maximum (Pmax) was based on the maximum willingness to pay for each consuming industry, which was assumed to take place when an industry’s entire value added was reduced to zero owing to the price increase of the mineral commodity consumed. The price maximum for each industry was therefore determined by setting equation 13 to zero:

An overall price maximum for each mineral commodity was determined to be the largest of the calculated industry price maximums that achieved market clearing based on the mineral availability constraint. This price maximum was ultimately only necessary for four mineral commodity scenarios: trade disruption from China of lutetium, samarium, thulium, and ytterbium.

The postdisruption value added for producing industries was calculated in a similar manner to that of consuming industries except that the price effect increased rather than decreased the industry’s value added, and a mineral production ratio (r) was used instead of a mineral consumption ratio:

Like the mineral consumption ratio, the mineral production ratio was calculated as the ratio of the predisruption mineral production quantity of that industry to its output in U.S. dollars. As with mineral consuming BEA industries, each mineral producing BEA industry (identified in appendix 1) was split into two industries: one that was directly associated with the mineral commodity’s production and the other that represented the remainder of the BEA industry. The monetary value of the production of the mineral commodity as a percent of the industry’s output was the basis for splitting the mineral commodity producing BEA industries. Note that the predisruption price used for domestic production (noted in appendix 3), which was used for splitting the BEA producing industries and calculating the value added of producing industries in equation 15, was not necessarily the same as the predisruption consumption price used in splitting the consuming BEA industries and calculating the value added of consuming industries in equation 13. This price difference reflects the fact that the predisruption domestic consumption prices were based on the unit value of domestic apparent consumption, which accounted for the value and quantity of not only domestic production but also net imports. Differences in production and consumption prices were mainly a reflection of the differences in the commodity forms produced and consumed domestically. Although the predisruption consumption and production prices were different, they were both increased postdisruption at the same rate using the price ratio that was calculated in the equilibrium displacement model (or the calculated price maximum).

As with the mineral commodity availability constraint (eq. 10), a mineral commodity production constraint was included in the optimization routine to match the equilibrium displacement model results:

As illustrated in equation 16, domestic production (ψUS) of the mineral commodity was assumed to grow at the same rate as the production of the rest of the world but was limited by the maximum reported or estimated capacity of production in the United States, κUS. This constraint only applied to mineral commodities for which the United States was a producer. Note that because of this growth in domestic mineral commodity production, it was necessary in certain scenarios to remove the industry output capacity constraint (xci) for the producing industries.

The postdisruption value added for all other industries (meaning those that were neither direct consumers nor producers of the mineral commodity in question) were calculated without the price effect term of equations 13 and 15:

This approach assumed that direct consuming industries absorbed the entire price increase, with none of the price increase being passed on to downstream industries or final consumers. This assumption is not wholly realistic in all cases as many industries have the market power to pass through price increases, but it may be a reasonable assumption in the short term. These non-producing, non-direct consuming industries would thus be affected by the disruption indirectly through the IO tables and the objective function (eqs. 7–9), which seeks to minimize changes to not only each industry’s value added but also each interindustry intermediate and final demand.

Increases in prices of mineral commodities were accounted for only in the value added variable and not the other variables (industry output, final demand, or interindustry intermediate demand). This approach allowed the IO model to remain in price equilibrium for all other goods and services, while still accounting for the effect of mineral commodities’ price increases on U.S. GDP.

The overall economic effect, or net decrease in U.S. GDP, was calculated as the sum of the changes in value added across all industries for a single scenario:

Note that in equation 18, a net decrease in U.S. GDP is presented as a positive value.

Model Implementation

To solve the convex optimization problem at the core of the economic impacts model, we used the Clarabel solver (Goulart and Chen, 2024), an interior-point method designed for second-order cone and quadratic programming. Clarabel was written in the Rust programming language and integrated through Python via CVXPY (2025), allowing for both speed and ease of embedding in high-level modeling workflows. Unlike some legacy solvers, it offers better handling of problem scaling and numerical precision, which can be especially important for economic applications involving large IO models. For model implementation, we used Python version 3.11.8 (Python Software Foundation, 2024), along with CVXPY version 1.6.5. Additional details are provided in appendix 5.

For each scenario, results included the postdisruption values for each industry’s output, interindustry intermediate demand, final demand, and value added. As noted earlier, the results for the newly formed industries were remerged after running the optimization routine in order to report the results across a consistent set of 402 industries. Additionally, net decreases in U.S. GDP were grouped into one of the following economic effects components: consuming industries reducing their output, consuming industries paying higher prices, producing industries increasing their output, producing industries receiving higher prices, and all other industries reducing their output.

Scenario Probabilities

Because not all scenarios are equally likely to occur, we estimated a probability for the occurrence of each scenario. The probability of an export restriction was set to 100 percent for 17 scenarios that represent China’s trade disruptions of the mineral commodities (antimony, bismuth, dysprosium, gadolinium, gallium, germanium, natural graphite, synthetic graphite, indium, lutetium, magnesium metal, molybdenum, samarium, tellurium, terbium, tungsten, and yttrium) that China’s MOFCOM has (as of this writing) explicitly identified as being either restricted or completely banned from being exported to the United States (Ministry of Commerce of the People’s Republic of China, 2024, 2025a, b). For all other scenarios, the probability of a country implementing a trade restriction on a given mineral commodity was obtained using the method developed in Ryter and Nassar (2025). These probabilities were calculated using an ensemble of several machine learning classifiers, each of which produced a probability estimate for each mineral commodity–country scenario. Exogenous variables such as prior trade barrier implementation (specifically, trade prohibition, quota, or licensing requirements) and global export dominance or dependence were used to train each classifier and inform its probability estimates. The median of the probabilities for the mineral production process or trade codes that most closely aligned with those selected in this analysis were used. Probabilities were unavailable for a few mineral commodity–country pairs. These pairs represent a small number (17 out of 1,205 scenarios) of low economic impact (with net decreases in U.S. GDP averaging less than $2 million) scenarios. For completeness, these scenarios were assigned a probability equal to the mean probability of all scenarios assessed (4 percent).

With the probabilities (ρ) assigned to each scenario, the expected value or probability-weighted net decrease in U.S. GDP across all scenarios (E[∆GDP]) for each mineral commodity was determined, as follows:

Risk Categorization

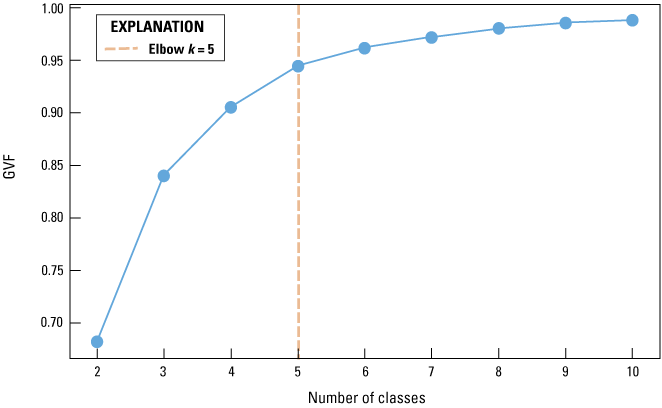

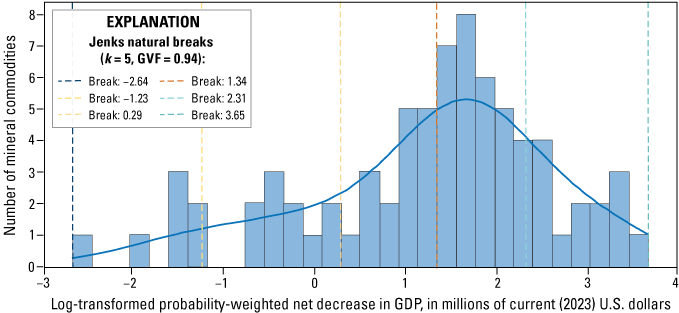

A statistical approach was used to categorize the risk results. Specifically, the classification of the probability-weighted net decrease in U.S. GDP was conducted using the Jenks natural breaks optimization method (Jenks, 1967), which aims to minimize variance within classes while maximizing variance between classes. This method provides optimized cutoff points based on the specified number of classes, allowing for differentiation between various economic effects. To determine the appropriate number of classes and avoid overfitting, the elbow method suggested by Satopaa and others (2011) was employed. Additional details are provided in appendix 6.

Results and Discussion

With 84 mineral commodities, 402 industries, and over 1,200 scenarios, the results of the analysis, which include changes in equilibrium prices and quantities, as well as changes in each industry’s output, interindustry intermediate demand, final demand, and contributions to U.S. GDP are too numerous to display and discuss in full in this report. Instead, below is a sampling of results for a single example mineral commodity, palladium (fig. 1), followed by a summary of the main result variable (the probability-weighted net decrease in U.S. GDP, which is presented as a positive value) for all mineral commodities by trade disruption scenario (table 1 and fig. 2), industry (table 2), and economic effects component (table 3). Palladium was selected as the example to present because it was one of only a few mineral commodities examined for which more than one trade disruption scenario contributed notably to its overall probability-weighted net decrease in U.S. GDP.

Results for Palladium

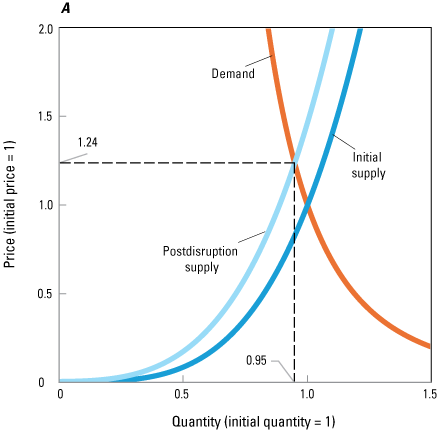

In figure 1A, the estimated supply and demand curves for palladium are displayed for a scenario in which U.S. net imports of palladium from Russia (a leading world producer and import source for the United States) were completely restricted for an entire year. The results indicate that the price would increase by 24 percent and the quantity available postdisruption would decrease by approximately 5 percent (the net disruption level, n′). This does not account for speculative (often temporary) price fluctuations in the cash market, but rather reflects the change in the modeled equilibrium price that would be expected from the supply shift. Excess production capacity in other producing countries, especially in South Africa, and inelastic demand were the main reasons that the net disruption level was not higher.

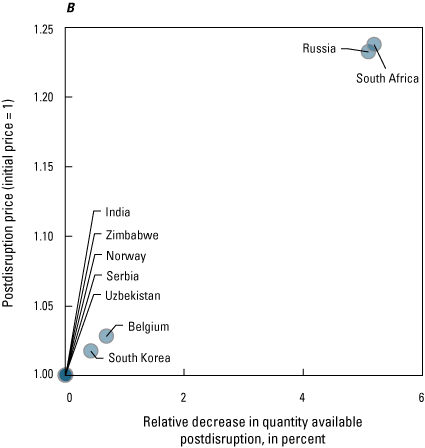

Displayed as a scatter plot, figure 1B illustrates the postdisruption prices and net disruption levels for all palladium scenarios (defined by the complete restriction of U.S. net imports of palladium from nine producers from which the United States was a direct or indirect net importer: Belgium, India, Norway, Russia, Serbia, South Africa, South Korea, Uzbekistan, and Zimbabwe). The results for South African and Russian scenarios were of similar magnitude, which is to be expected given that both countries produced and net exported to the United States roughly the same amount of palladium in 2023. The availability of Russian palladium helped to mitigate the effects of a South African disruption just as the availability of South African palladium helped to mitigate the effects of a Russian disruption. A scenario in which South Africa and Russia disrupted palladium trade simultaneously was not modeled but would have undoubtedly resulted in a markedly higher disruption level and price given the lack of substantial production outside of these two countries. In contrast, disruption scenarios for Belgium and South Korea, both of which refined and recycled but did not mine palladium, resulted in markedly lower net disruption levels and price increases. These smaller decreases correspond to not only lower U.S. net imports from these countries but also a larger quantity of palladium available from other countries, mainly Russia and South Africa. The impacts from the remaining five scenarios (India, Norway, Serbia, Uzbekistan, and Zimbabwe) were even less pronounced, with extremely low net disruption levels and price increases, primarily due to their markedly smaller contributions to U.S. net imports of palladium and the availability of palladium from major producers like Russia and South Africa. Scenarios from other palladium producers (for example, Canada) were excluded from the analysis because the United States was a net exporter of palladium to those producers in 2023.

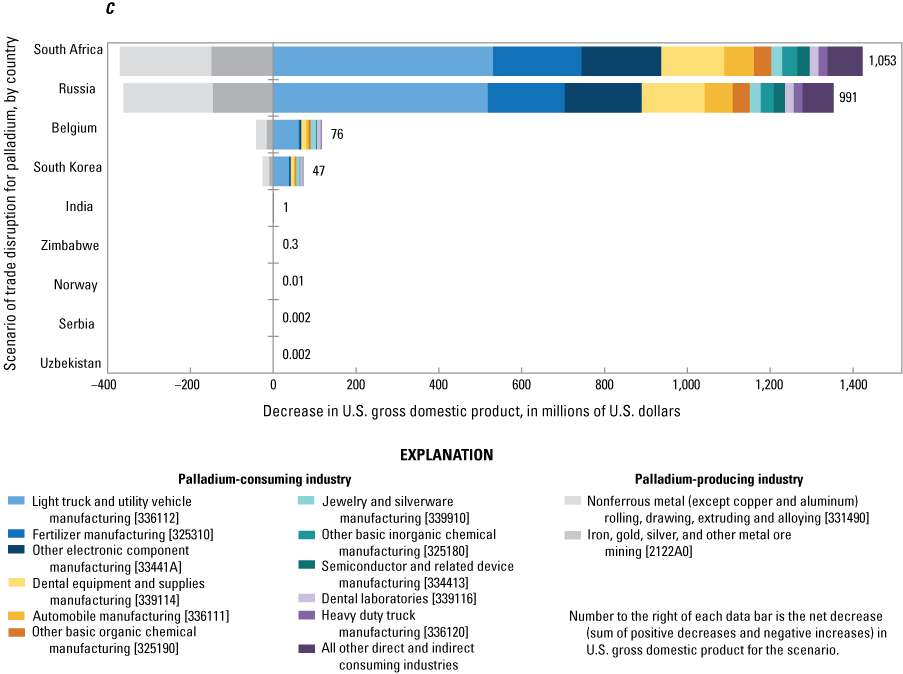

Four graphs showing various results from modeling trade disruption scenarios (the restriction of U.S. net imports from producers from which the United States was a direct or indirect net importer) for palladium. A, estimated palladium supply and demand curves for the rest of the world under a trade disruption scenario in which U.S. net imports of palladium from Russia were completely restricted for an entire year. Demand remaining constant, the supply curve shifts postdisruption, causing the postdisruption price to increase and quantity to decrease. B, estimated postdisruption price increase and relative decrease in quantity available postdisruption under nine trade disruption scenarios for palladium (the restriction of U.S. net imports of palladium from nine producers from which the United States was a direct or indirect net importer: Belgium, India, Norway, Russia, Serbia, South Africa, South Korea, Uzbekistan, and Zimbabwe). C, net decreases in U.S. gross domestic product (GDP) by industry under nine trade disruption scenarios for palladium. Industries shown are those industries that had the highest contributions to the net decrease in U.S. GDP for palladium across the nine scenarios. Each industry is followed by a 6‑character alphanumeric code from the U.S. Bureau of Economic Analysis in brackets. Values represent the effect for each scenario in current (2023) U.S. dollars, but not do reflect the probability of occurrence. Negative values indicate an increase in U.S. GDP by a given industry. Number to the right of each data bar is the net decrease (sum of positive decreases and negative increases) in U.S. GDP for the scenario. The scenarios are listed in descending order of net decrease. D, estimated median probability of scenario occurrence and net decreases in U.S. GDP for nine trade disruption scenarios for palladium. Five scenarios have net decreases too small to be legible on the figure. Probability-weighted net decreases in U.S. GDP (the product of the modeled net decrease for the scenario and its probability of occurrence) are represented as the area of each scenario with the value being displayed (in millions of U.S. dollars) below the country name for each scenario. The total area (across all scenarios) represents the overall probability-weighted net decrease in U.S. GDP for palladium. Scenarios are shown consecutively along the horizontal axis in descending order by the probability of the scenario occurring to show the relative contribution of the given scenarios to the overall probability-weighted net decrease in U.S. GDP.

Results from the economic impacts modeling for all nine palladium scenarios by industry are displayed in figure 1C. Specifically, this part of the figure displays the modeled effects on U.S. GDP for 11 palladium-consuming industries that contributed the most to the decreases along with increases to U.S. GDP from 2 palladium-producing industries (mining and recycling) and an “all other industries” category that reflects the aggregate effect on the remaining 389 industries, which includes several additional industries that were direct consumers of palladium. All changes in U.S. GDP are presented in current (2023) U.S. dollars. Scenarios of Russian and South African palladium trade disruptions resulted in the largest net decreases in U.S. GDP (displayed in the data labels of each scenario in figure 1C) of approximately $1 billion each, whereas the scenarios for Belgium and South Korea both resulted in net decreases of less than $100 million and those from the five other scenarios resulted in net decreases of $1 million or less. Although the specific industry contributions to the decreases varied by scenario, the industries that contributed the most overall were the “Light truck and utility vehicle manufacturing [336112]” industry, where palladium is used in catalytic converters; the “Fertilizer manufacturing [325310]” industry, where palladium is used as a catchment gauze in nitric acid production; and the “Other electronic components manufacturing [33441A]” industry, where palladium is used in multilayer ceramic capacitors. The other industries affected reflect palladium’s use in dental alloys, hybrid integrated circuits, jewelry, catalytic converters for other vehicle classes, and catalysts for other chemical industries. In these scenarios of foreign supply disruptions, palladium-producing industries (under BEA industry code 2122A0 for mining and 331490 for recycling) garnered higher palladium prices and increased their palladium production, thereby increasing their positive contribution to U.S. GDP, which reduced the net effect of the trade disruptions on the economy overall.

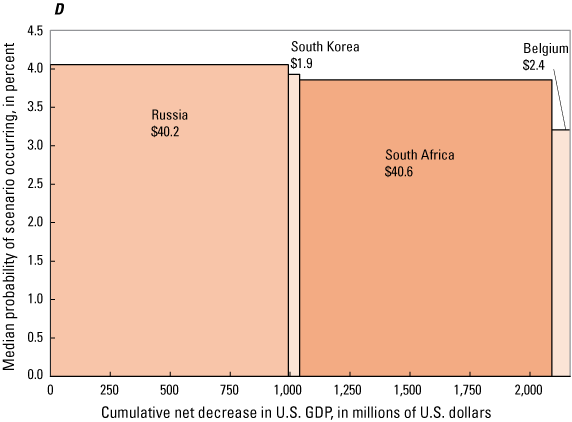

Figure 1D displays the results of the economic impacts model for each scenario (horizontal axis) and the median probability of the scenario occurring (vertical axis) based on the analysis conducted by Ryter and Nassar (2025). In this variable-width column graph, the area of each scenario (the product of the median probability and the net decrease in U.S. GDP) represents the probability-weighted net decrease in U.S. GDP. Although the South African scenario resulted in the largest decrease of U.S. GDP (as also displayed in figure 1C), its probability of occurrence (approximately 3.9 percent) was slightly lower than of the Russian scenario (approximately 4.1 percent). The probability of Russia restricting palladium supplies might seem low given recent geopolitical tensions but is attributable to the relative infrequency with which Russia imposes export restrictions on mineral commodities, which may be a reflection of their importance as a revenue source (Ryter and Nassar, 2025). Additionally, the scenarios do not account for any current or potential U.S.-imposed import sanctions. Nevertheless, the contribution of the Russian scenario (the product of the scenario’s impact and probability represented by the area of the scenario) to the overall probability-weighted net decrease in U.S. GDP was slightly smaller ($40.2 million) than that of the South African scenario ($40.6 million). The contributions to the probability-weighted net decrease in U.S. GDP from the South Korean and Belgian scenarios were both lower. Although the other 5 scenarios are displayed in figure 1D, they are too small (on the horizontal axis) to be legible. The probability-weighted net decrease in U.S. GDP across all scenarios, the entirety of the shaded area of figure 1D, totaled approximately $85 million.

Results by Trade Disruption Scenario

A summary of the contributions to the probability-weighted net decrease in U.S. GDP for each mineral commodity by leading country contribution is provided in table 1. The results indicate that samarium has the largest overall probability-weighted net decrease in U.S. GDP of nearly $4.5 billion. This modeled economic impact comes almost entirely from the China disruption scenario, for which a probability of 100 percent was used because of the recent export restriction. Several of the other “middle” and “heavy” rare earth elements (that is, lutetium, terbium, dysprosium, gadolinium, and yttrium) were also determined to have among the largest probability-weighted net decreases in U.S. GDP among all the mineral commodities examined, owing to the near complete lack of production of these mineral commodities outside of China. China was the leading contributor to the probability-weighted net decrease in U.S. GDP of 46 of the 84 mineral commodities examined, including all the rare earth elements, gallium, germanium, tungsten, and magnesium metal. Canada and South Africa were each the leading contributor to the probability-weighted net decrease in U.S. GDP for eight mineral commodities including potash, aluminum, and zinc (smelted) for Canada and rhodium, platinum, ruthenium, iridium, and chromium ferroalloys for South Africa. Most (at least 50 percent) of the contributions to the probability-weighted net decrease in U.S. GDP come from a single scenario for 65 out of the 76 mineral commodities that had positive probability-weighted net decreases in U.S. GDP—a reflection of the high degree of country-level concentration of both world production and U.S. imports.

Table 1.

Probability-weighted net decreases in U.S. gross domestic product (GDP), by scenario across all industries, and scenario contributing most to the probability-weighted net decrease in U.S. GDP for each mineral commodity.[Mineral commodities are listed in order of overall probability-weighted net decrease in U.S. GDP. Scenarios shown are the disruption of U.S. net imports of the mineral commodities from 12 producers from which the United States was a net importer that resulted in the greatest probability-weighted net decrease in U.S. GDP across the mineral commodities examined: Australia, Belgium, Brazil, Canada, Chile, China, Germany, India, Malaysia, Mexico, Russia, South Africa. All other scenarios are aggregated under the “all other countries” column. Probability-weighted net decreases are the product of the net decrease in U.S. GDP of the scenario and its median probability of occurrence. Results are in current (2023) U.S. dollars and were rounded to the nearest million U.S. dollars; may not add to totals shown. Probability-weighted net decrease values are gradationally shaded between the 5th and 95th percentiles of the values in the table to visually highlight positive (orange) to negative (blue) values. For mineral commodities with an overall negative net decrease (meaning those with an overall net increase) in U.S. GDP, the scenario contributing the most to the net decrease is not displayed. %, percent; —, indicates that the scenario was not applicable for that mineral commodity]

Summing the economic impact across mineral commodities should not be viewed as the potential effect of simultaneous disruptions across multiple mineral commodities, as such a scenario may have notably different results owing to the interactions between the industries and mineral commodities involved.

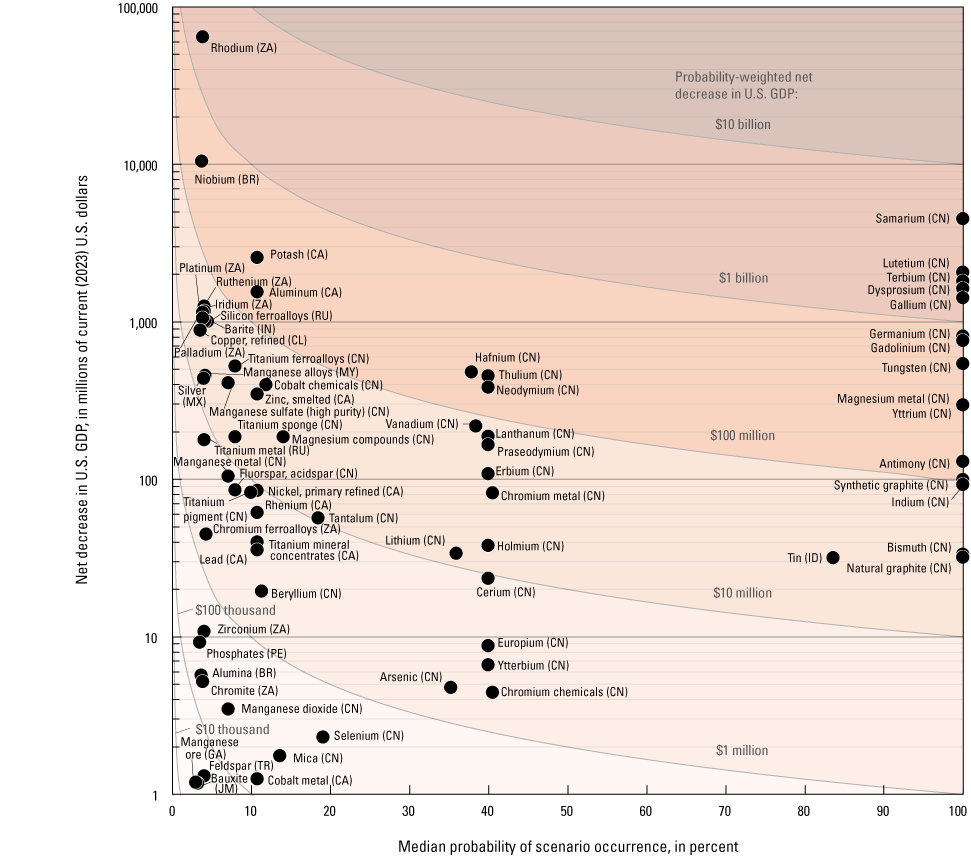

Graph showing net decreases in U.S. gross domestic product (GDP) and median probability of occurrence for the leading trade disruption scenario for 72 of the 84 mineral commodities examined. Scenarios with net decreases less than $1 million are not displayed. Vertical axis is displayed in a logarithmic scale. The gray curves are used to provide a visual reference for the resultant probability-weighted net decreases in U.S. GDP (the product of the net decrease in U.S. GDP of the scenario and its median probability) at several different orders of magnitude, and intervals between the curves are shaded to help visually group scenarios of similar magnitudes. Point labels display the mineral commodity and (where necessary) the supply chain process or chemical form, followed by the restricting country in parentheses, shown using each country's 2‑letter ISO 3166 country code, as follows: BR, Brazil; CA, Canada; CL, Chile; CN, China; GA, Gabon; ID, Indonesia; IN, India; JM, Jamaica; MX, Mexico; MY, Malaysia; PE, Peru; RU, Russia; TR, Turkey; ZA, South Africa.

If a specific disruption scenario were to take place, its impact would be greater than the probability-weighted value. For example, the modeled South African trade disruption of rhodium was estimated to result in a net decrease of over $64 billion in U.S. GDP. However, because the probability of such an occurrence is 3.9 percent, the probability-weighted decrease was just under $2.5 billion. Similarly, a niobium disruption from Brazil was estimated to result in a net decrease of over $10.4 billion in U.S. GDP, but the estimated probability of occurrence is 3.7 percent. This is more clearly displayed in figure 2, which plots the effect (net decreases) on U.S. GDP (vertical axis) and the median probability of occurrence (horizontal axis) for the leading scenario for each mineral commodity. Scenarios with net decreases less than $1 million are not displayed in figure 2. Figure 2 only displays the scenario with largest net decrease in U.S. GDP for each mineral commodity. Only one scenario is thus displayed for each mineral commodity even if that mineral commodity has more than one scenario with net decreases over $1 million. Consequently, figure 2 does not display the mineral commodity’s overall probability-weighted net decrease in U.S. GDP across all scenarios.

Results by Industry

Table 2 displays the same probability-weighted net decrease in U.S. GDP for each mineral commodity as table 1 but now by leading contributing industry. This figure highlights that samarium’s probability-weighted net decrease in U.S. GDP was mainly driven by the “Guided missile and space vehicle manufacturing [336414]” and the “Search, detection, and navigation instruments manufacturing [334511]” industries. The “Search, detection, and navigation instruments manufacturing [334511]” industry was also a notable contributor to the probability-weighted net decrease in U.S. GDP for germanium. The largest contributing industry to the probability-weighted net decrease in U.S. GDP for germanium was, however, the “Semiconductor and related device manufacturing [334413]” industry, which was also a leading contributor to the probability-weighted net decrease in U.S. GDP for gallium, lutetium, and thulium. The “Electric lamp bulb and part manufacturing [335110]” industry was the largest contributor to the probability-weighted net decrease in U.S. GDP for terbium, gadolinium, and yttrium, where these mineral commodities are used as phosphors. A large contributor to the probability-weighted net decrease in U.S. GDP decline for terbium and other rare earths used in permanent magnets (dysprosium, gadolinium, neodymium, and praseodymium) was the “Audio and video equipment manufacturing [334300]” industry.

Table 2.

Probability-weighted net decrease in U.S. gross domestic product (GDP) by industry across all scenarios, and industry contributing most to probability-weighted net decrease in U.S. GDP for each mineral commodity.[Mineral commodities are listed in order of overall probability-weighted net decrease in U.S. GDP. Only the 10 industries that contributed the most (in descending order from left to right) to the probability-weighted net decrease in U.S. GDP across all mineral commodities are displayed. The probability-weighted net decrease in U.S. GDP for the remaining 392 industries are aggregated under the “all other industries” category. Each industry name is followed by a 6-character alphanumeric code from the U.S. Bureau of Economic Analysis in brackets. Results are in current (2023) U.S. dollars and were rounded to the nearest million U.S. dollars; may not add to totals shown. Probability-weighted net decrease values are gradationally shaded between the 5th and 95th percentiles of the values in the table to visually highlight positive (orange) to negative (blue) values. mfg., manufacturing]

These results are as much a reflection of the scenarios (and the probability of each scenario’s occurrence) as they are of the importance of the mineral commodity to the identified industry. For example, neodymium and praseodymium play prominent roles in permanent magnets, perhaps more so than samarium. However, the disruption scenarios for these two rare earth elements yielded notably lower impacts than those of the other rare earth elements used in permanent magnets owing to the increased production of separated “light” rare earth elements outside of China in recent years. Similarly, lutetium has a very limited role (as a cracking catalyst) in petroleum refining, in contrast to palladium, platinum, and rhenium. The notable contribution to lutetium’s probability-weighted net decrease in U.S. GDP from that industry is thus more of a reflection of that scenario (in which virtually no lutetium production exists outside of China) than of lutetium’s importance to the petroleum refining industry. Moreover, because of extremely inelastic supply and demand, a large portion of the probability-weighted net decrease in U.S. GDP for lutetium was modeled to come from the consuming industry paying higher prices.

Results by Economic Effects Component

The effect of consuming industries paying higher prices is more clearly reflected in table 3, which summarizes the probability-weighted net decrease in U.S. GDP for the following economic effects components: consuming industries reducing their output, consuming industries paying higher prices, producing industries increasing their output, producing industries receiving higher prices, and all other industries reducing their output. Displaying the results by component highlights the role of price elasticities and the availability of excess production capacity outside of the restricting country in the analysis. Approximately one-half of samarium’s probability-weighted net decrease in U.S. GDP was due to consuming industries paying higher prices. Consuming industries paying higher prices was a major contributor to the probability-weighted net decrease in U.S. GDP for several other mineral commodities including aluminum, antimony, copper (refined), gold, lead, neodymium, potash, rhodium, silver, tungsten, and zinc (smelted). In contrast, consuming industries reducing their output was a larger contributor to the probability-weighted net decrease in U.S. GDP for most of the other mineral commodities with large probability-weighted net decreases in U.S. GDP including, dysprosium, gadolinium, gallium, germanium, hafnium, magnesium metal, niobium, terbium, and yttrium.

Table 3.

Probability-weighted net decrease in U.S. gross domestic product (GDP) by economic effects component (net decrease in U.S. GDP owing to changes in industry outputs or higher mineral commodity prices).[Mineral commodities are listed in order of overall probability-weighted net decrease in U.S. GDP. Results are in current (2023) U.S. dollars and were rounded to the nearest million U.S. dollars; may not add to totals shown. Probability-weighted net decrease values are gradationally shaded between the 5th and 95th percentiles of the values in the table to visually highlight positive (orange) to negative (blue) values. —, no domestic producers of the mineral commodity]

Table 3 also provides insights into the availability or lack of domestic production. As noted earlier, under scenarios of foreign trade disruptions, domestic producers of the mineral commodity benefit from higher prices and increased output. For all mineral commodities examined, domestic producers benefited more from higher prices than from increased output. This was especially the case for producers of aluminum, copper (refined), gold, lead, rhodium, and tungsten. For gold, the higher prices that domestic producers would be expected to receive more than offset the expected decreases in U.S. GDP attributable to lower outputs of and higher prices paid by consuming industries.

The impact on all other industries (those that are not direct consumers or producers of the mineral commodity) varies notably by mineral commodity and reflects how downstream industries may be affected. One factor that may have affected these results was whether the mineral commodity was consumed as a final good (as reflected in final demand) or was mainly an input for downstream manufacturers (as reflected in interindustry intermediate demand). Several of the mineral commodity alloys (for example, manganese alloys, silicon ferroalloys, and titanium ferroalloys) have much larger contributions to the probability-weighted net decreases in U.S. GDP from downstream industries rather than from direct consuming industries. For some mineral commodities, the contributions to the probability-weighted net decrease in U.S. GDP was negative for both the consuming industries and all other industries, reflecting a net increase in their overall economic activity. Note that these are aggregate results (across various industries and scenarios) and can be attributed to the optimization routine finding an optimal solution that allowed some industries to increase their economic activity while satisfying the specified constraints on mineral commodity availability and industry output capacity. This economic adjustment would occur when industries with relatively high contributions to U.S. GDP per unit of mineral commodity consumption increased their output while industries with lower contributions reduced their output even more, thereby reducing the overall consumption of the mineral commodity and meeting the mineral availability constraint of the scenario. These tradeoffs between industries were limited by the objective function of the optimization routine, which sought to minimize change. In practical terms, these net increases in U.S. GDP from direct and indirect consuming industries reflects the ability of industries to adjust their economic activities in response to the trade disruption scenario.

Summary of Results and Recommendations

Table 4 provides a summary of the key results (the probability-weighted net decreases in U.S. GDP for each mineral commodity examined) and recommendations for each mineral commodity’s inclusion on the LCM. The results largely reflect the following factors:

-

1. the concentration of U.S. net imports from countries likely to prohibit exports,

-

2. the size of U.S. imports as a share of production outside of the restricting country,

-

3. the import dependence of the United States,

-

4. the availability of excess capacity outside of the restricting country,

-

5. the responsiveness (elasticity) of supply and demand in the short term (within 1 year), and

-

6. the economic value of the (direct and indirect) consuming and producing industries’ contributions to the U.S. economy.

Table 4.

Overview of mineral commodity assessment, ranking, and categorization for inclusion on the draft List of Critical Minerals (LCM) in 2025.[Mineral commodities are listed in order of overall probability-weighted net decrease in U.S. gross domestic product (GDP). Mineral commodities that were not evaluated using the quantitative assessment were not ranked (ranking represented by a dash, —) and are ordered alphabetically after those ranked. Results are in current (2023) U.S. dollars and were rounded to the nearest million U.S. dollars; may not add to totals shown. Statistical risk categories were determined based on the probability-weighted net decreases in U.S. GDP (in millions of U.S. dollars) in rounded intervals, as follows: high, >206; elevated, >22 to 206; moderate, >2 to 22; limited, >0.06 to 2; negligible, 0 to 0.06; negative, <0. A mineral commodity was recommended for inclusion on the updated LCM if the probability-weighted net decrease in U.S. GDP decline was determined to be at or above the “moderate” risk category in any process of the domestic supply chain (or chemical form) or if the mineral commodity had a single point of failure (SPOF) in the supply chain. Probability-weighted net decrease values and their corresponding risk categories are shaded according to their risk category classification: high to limited are shaded in progressively lighter shades of orange; negligible are white; and negative are blue. Mineral commodity forms and supply chain processes not previously assessed separately are marked with an asterisk in the final column]

As described in the “Methods” section, statistical risk categories were determined based on the Jenks natural breaks optimization method. The results of that statistical method indicate that the probability-weighted net decreases in U.S. GDP for the 84 mineral commodities examined can be classified into five risk classes or categories (after excluding the mineral commodities with overall net increases to the probability-weighted U.S. GDP, indicated as “negative” in table 4). These risk categories, as shown in table 4, had the following descriptors and ranges of probability-weighted net decreases (in millions of current [2023] U.S. dollars): “negligible,” 0 to 0.06; “limited,” >0.06 to 2; “moderate,” >2 to 22; “elevated,” >22 to 206; and “high,” >206.

Based on the first criterion, mineral commodities are recommended be included on the updated LCM if the probability-weighted net decrease in U.S. GDP decline was found to be at or above the “moderate” risk category in any stage of the supply chain (or chemical form). With two risk categories above and two risk categories below, selecting the “moderate” risk category prevents the exclusion of mineral commodities with notable risks (those with probability-weighted net decreases in U.S. GDP in the tens of millions of current [2023] U.S. dollars) and avoids the inclusion of those with risks that are likely too low for consequential policy consideration (those with probability-weighted net decreases in U.S. GDP in the hundreds of thousands of U.S. dollars and up to $2 million). Policymakers and other users who use the LCM may, however, elect to use a different minimum risk category (for example, “elevated”) or a specific monetary cutoff value (for example, $100 million) that corresponds to a specific risk tolerance or meets the definition of “significant consequences” outlined in the Energy Act of 2020.

The second criterion was if the mineral commodity had a SPOF. Although several mineral commodities currently have a SPOF, it was only necessary to apply this criterion to zirconium given that the other mineral commodities had risk ratings categorized as being “moderate” or higher. Although there were two firms that recovered zircon—the primary source of zirconium—from heavy-mineral sands and two firms that produced zirconium metal (U.S. Geological Survey, 2025a), there was only one domestic producer of fused zircon and no domestic producer of zirconium oxychloride, both of which were necessary precursors for zirconium metal (Nassar and Fortier, 2021; U.S. Trade Representative, 2019).

In comparison to the previous LCM from 2022, several additional mineral commodities are now recommended for inclusion (in descending order of risk as determined in this assessment): potash, silicon (in particular, silicon ferroalloys), copper (in particular, refined copper), silver, rhenium, and lead. Although global potash production was not as highly concentrated as some other mineral commodities, the vast majority (approximately 90 percent) of U.S. net imports of potash were obtained from a single country, Canada, in 2023. Potash’s relatively large probability-weighted net decrease in U.S. GDP is thus principally a reflection of the high degree of U.S. dependency on Canada (refer to table 1 and fig. 2). In contrast to the low disruption probabilities for Russia and South Africa, Canada’s disruption probability for several mineral commodities is relatively high (for example, just under 11 percent for potash). This comparatively elevated probability can be attributed to Canada’s relatively high rate of historical trade barrier implementation. Between 1989 and 2023, Canada implemented prohibition, quota, or licensing requirements on mineral commodities in 8 different years, whereas other key mineral commodity-producing countries such as Russia and South Africa have implemented such barriers in only 6 and 4 different years, respectively (Ryter and Nassar, 2025). Even if the probability of a Canadian potash trade disruption scenario occurring was an order magnitude lower than estimated (for example, 1.1 percent instead of 11 percent), the overall probability-weighted net decrease in U.S. GDP for potash would still be considerably higher (around $41 million after accounting for not only the assumed lower probability for the Canadian scenario but also all the other scenarios at the estimated probabilities) than the minimum value required to meet the “moderate” risk category of greater than $2 million. Silver’s probability-weighted net decrease in U.S. GDP is largely due to a scenario in which Mexico stops silver exports to the United States—a high impact ($435 million), low probability (4 percent) event (refer to table 1 and fig. 2). In the previous LCM assessment (Nassar and Fortier, 2021), lead and rhenium were both just below the cutoff threshold for recommendation to the LCM, whereas the risk for refined copper was trending upward. The evaluation of lead and rhenium just above the minimum threshold of this assessment underscores the idea that risk assessments operate on a continuum. Evaluating a mineral commodity just above and subsequently just below a threshold in consecutive assessments may also warrant the retention of the mineral commodity on the LCM for additional time to allow for stability in policymaking. Silicon metal and mined copper have negative probability-weighted net decreases in U.S. GDP but are still recommended for inclusion because of the risks associated with other stages of their supply chains, namely silicon ferroalloys and refined copper. Their negative probability-weighted net decreases in U.S. GDP were due to the United States being a net exporter of copper ores and concentrates and exporting higher value (and higher grades of) silicon metal (polysilicon) than it imports.

Arsenic and tellurium, both of which were included on the previous LCM in 2022, do not qualify under either criterion of this assessment. With the recent installation of copper telluride recovery capability by a major copper operation in Utah (Rio Tinto plc, 2022), the United States has moved from being over 95 percent net import reliant in 2021 to being a net exporter of tellurium in 2023 (U.S. Geological Survey, 2025a). Although the domestically produced copper telluride was not refined in the United States, the notable reduction of U.S. imports of tellurium since 2022 (U.S. Geological Survey, 2025a) has resulted in a decrease in tellurium’s supply risk from foreign trade disruptions. However, that risk may return if one or both current domestic producers stop recovering copper telluride or if world tellurium production becomes even more geopolitically concentrated despite the notable enrichment (but lack of recovery) of tellurium within the copper anode slimes of copper electrolytic refineries (Nassar and others, 2022). Although the United States obtains most of its arsenic from China, revised data from the USGS (U.S. Geological Survey, 2025b) indicates that Peru (not China) was the leading producer of arsenic. Even though arsenic remains important for its use in gallium arsenide wafers, a greater concern in that supply chain is China’s dominance in primary gallium production (Nassar and others, 2024).

As with the previous LCM assessment, there were insufficient data to quantitatively evaluate the risks for cesium, rubidium, and scandium. Although they have limited commercial applications, the United States has continued to be completely import reliant for all three mineral commodities (U.S. Geological Survey, 2025a). Moreover, scandium is specifically called out for export restriction by China’s MOFCOM (Ministry of Commerce of the People’s Republic of China, 2025b). There was insufficient justification for changing their status on the LCM, but future assessments could strive to quantitively assess their risk.

Conclusions

The results of the economic effects assessment and the SPOF criteria recommend the addition of six mineral commodities (in descending risk order, potash, silicon, copper, silver, rhenium, and lead) to the LCM and the removal of two mineral commodities (arsenic and tellurium) from the LCM. These recommendations are based on a statistical approach that classifies the probability-weighted economic effects into specific quantitative intervals. In determining the final LCM or in using the results of this methodology, decisionmakers may wish to consider other thresholds based on a specific risk tolerance, examine other risks (for example, the potential for supply disruptions from natural hazards [Jaiswal and others, 2024]), or address other considerations (for example, future demand expectations or the strategic importance of certain industries beyond economic valuation). Moreover, although defense-related industries are captured in the IO tables, consequences to the national security of the United States beyond economic effects are not directly factored into this analysis but may be addressed in the final LCM through consultation with the heads of other relevant executive departments and agencies as indicated by the Energy Act of 2020. Additionally, postponing the removal of mineral commodities may provide sufficient time for current policies to achieve their intended effects. For example, the Secretary of the Interior may decide to remove a mineral commodity now or wait to see if it is again recommended for removal in the next cycle. The assessment of risk exists on a continuum and this may influence decisions for mineral commodities near thresholds of evaluation. Mineral commodities with the highest probability-weighted net decreases in U.S. GDP may warrant closer evaluation and prompt greater attention from policymakers and other users of this information than those with low or negative probability-weighted net decreases in U.S. GDP. Several of the mineral commodities with the highest estimated risk have not only received attention but also action by the U.S. Government and others. For example, earlier this year, an Australian company’s facility in Malaysia announced plans to expand its heavy rare earth separation circuit to produce dysprosium, holmium, and terbium concentrate (Govind, 2025) and has plans to build a plant with similar capabilities in the United States through Presidential directive under Defense Production Act Title III (U.S. Department of Defense, 2021). Additionally, a U.S. producer recently announced that it has entered a partnership with the U.S. Department of Defense to accelerate its U.S. rare earth mine-to-magnet supply chain (MP Materials Corp., 2025). These recent announcements are part of a years-long effort on the part of the U.S. Government and other governments around the world aimed at reducing the risks associated with rare earths and other critical mineral commodities (International Energy Agency, 2025).